Recent Blog

Category

Personal Finance

**💔 In 2025, even the Big 4 — Groww, Zerodha, AngelOne & Upstox — together lost 20 lakh users!**

👉 Just in August, over 7 lakh traders pressed EXIT! 🚪

🎢 Is the F&O Party Slowing Down? 🥂

Retail traders who once rushed into weekly options are now pulling back.

⚡️ High-risk thrills are fading.

⚖️ Regulations are tightening.

💸 Quick-money dreams → turning into losses.

**🏛 What Policymakers Did:**

🔺 Higher Margins → More capital needed.

📉 Less Expiries → Fewer thrill rides every week.

🚧 Entry Barriers Raised → Small traders squeezed out.

💰 Higher Taxes → Eating into short-term profits.

**📊 My Client Story**

👉 From my own experience as an MFD (Mutual Fund Distributor) — I’ve seen this shift first-hand.

📌 50% of the clients I onboarded this financial year came from discount brokers!

But when markets turned choppy, many realized that DIY trading isn’t always wealth creation.

That’s when they leaned on me for guidance:

🤝 Hand-holding in volatile times.

🛡 Helping control fear & greed.

📈 Keeping long-term wealth discipline intact.

💡 Showing opportunities beyond just “quick trades.”

**🔄 Where Are They Moving?**

💹 Equity Mutual Funds → Thematic & sectoral bets growing:

PSU 🚂 Infrastructure push.

Healthcare 🏥 Defensive, steady growth.

Consumption 🛒 India’s demand story driving FMCG, retail, lifestyle.

👨💼 PMS → Tailored wealth play for HNIs.

🏦 AIFs → Alternative routes gaining love.

📑 Managed Portfolios → Safer, low-stress investing.

**🌐 The Big Picture**

Retail’s “option trading masti” → slowing down ⏸️

Shift from speculation 🃏 → managed investing 📊

Brokers now eyeing Advisory | Wealth | MF Distribution.

**⏳ Is this a short pause… or a permanent structural shift? Time will tell.**

👤 Dinesh Aneja

📞 +91 8800203200

🌐 www.gycbydineshaneja.in

**💡 Helping you invest wisely, not wildly! 🚀**

Read More →

Category

Personal Finance

**Responsible Investing:**

The Pain in Mid- and Small-Caps Has Just Begun

Hello everyone,

As we step into 2025, I want to share some insights that are rooted in conversations with fund managers over training session, my own research, and interactions with many of you.

Responsible investing—a subject more relevant than ever given what we’re seeing in mid and small cap stocks.

Over the last few months, almost every fund manager I’ve spoken to has shared a bearish outlook on mid and small caps. Our independent research pointed to the same basis data collated at our end with backtesting results of last 5 years and Macros of the economy. This lead to the same conclusion, leading us to communicate caution and a reduction in exposure (Covered in Sept'24 Blog)

In my last quarter messages, I reiterated this. Yet many clients remain unfazed When Confidence Peaks, Caution Is Key.

This week, I met with an 60-plus-year-old client—a seasoned investor.

For months, I’ve been urging him to reduce his mid-small-cap exposure. Despite my warnings, he remains steadfast, armed with rationale after rationale for why this segment will perform well. His belief is unwavering, driven by a long-term view and recent market performance.

But let’s pause and reflect.

•When seasoned fund managers are nervous, why are individual investors super confident?

•Why do professional risk models flash red while retail investors see green lights?

•Why do they believe in TV stories and Fin influencers and not their own advisors/distributors?

**The Behavioral Trap:**

Recency Bias and Overconfidence

In investing, confidence often peaks just before trouble begins. The last few months felt like a vindication of retail investors’ decisions, as mid- and small-caps continued to rise. However, this false sense of security can blind us to looming risks.

Remember:

•Recency bias makes us believe that what worked recently will continue to work.

•Long-term investing doesn’t mean holding risky assets through a drawdown when market cycles clearly shift.

It’s true that small- and mid-cap companies have immense potential. But every investment must be viewed through the lens of valuation, market sentiment, and macroeconomic reality. Today, those signals suggest that the pain in mid- and small-caps has only just begun.

**What Responsible Investing Means Today**

1.Avoid chasing past winners:

Just because mid- and small-caps have done well doesn’t mean they’ll keep doing so.

2.Balance your portfolio: Diversification into large-cap and multi-cap strategies provides stability along with Debt Funds or hybrid funds.

3.Listen to professional guidance: Fund managers use data and experience to assess risks that aren’t always obvious.

Remember:

Volatility is temporary, but permanent loss of capital can derail your financial goals.

**Conclusion:**

Responsible investing is about managing risk as much as seeking returns. We believe this is a time to stay disciplined and follow a research-backed strategy, even if it feels counterintuitive. While short-term gains may tempt us to hold onto mid- and small-caps, the best investment decisions are often the hardest to make

If you’re feeling unsure about your portfolio exposure, we’re here to help. Let’s work together to ensure your investments align with your goals and today’s market realities.

Stay safe, stay diversified, and invest responsibly to garner the gains of India's long term Growth Story.

Regards,

GYC by Dinesh Aneja

+91 8800 203200

Read More →

Category

Personal Finance

From Fear to Fortune: A 10-20 Year Investment Odyssey

In 2008, market turmoil tested your resolve, but wisdom prevailed:

"Don't invest for 10-15%, invest for 10-15 times over 10-15 years. Think like an owner, not a tenant."

Post-35% Fall: A Fresh Start_

**Investment Strategy:**

- Invest ₹10,000/month

- Horizon: 10-20 years

- Asset Allocation: 60-80% Equity, 20-40% Debt

**Projected Growth (CAGR):_**

- 10 years: 12-15% CAGR ( ₹22.5 lakhs - ₹31.5 lakhs)

- 15 years: 15-18% CAGR ( ₹55 lakhs - ₹85 lakhs)

- 20 years: 18-20% CAGR ( ₹1.2 crores - ₹1.8 crores)

**Wealth Creation Milestones:**

- 5 years: ₹8 lakhs - ₹12 lakhs

- 10 years: ₹22.5 lakhs - ₹31.5 lakhs

- 15 years: ₹55 lakhs - ₹85 lakhs

- 20 years: ₹1.2 crores - ₹1.8 crores

**Growth Chart:**

| Year | Investment | Growth |

| --- | --- | --- |

| 5 | ₹6 lakhs | ₹8-12 L |

| 10 | ₹12 lakhs | ₹22.5-31.5 L |

| 15 | ₹18 lakhs | ₹55-85 L |

| 20 | ₹24 lakhs | ₹1.2-1.8 Crs |

**Investment Insights:**

- Consistency triumphs over timing

- Long-term focus beats short-term fears

- Equity investing rewards patience

**Gratitude and Guidance:**

Your mentor's wisdom transformed your investment approach. Now:

- Stay calm amidst market fluctuations

- Focus on wealth creation, not short-term gains

- Embody the owner's mindset, not the tenant's

**Celebrate Your Resilience:**

From fear to fortune, your investment journey has begun anew. Embrace the power of long-term investing.

***Additional Tips:***

- Rebalance portfolio periodically and do the sector rotation from long Term perspective

- Monitor and adjust asset allocation depending upon Macro's

- Stay informed, not emotionally invested

- Don't see your Mutual Fund Portfolio daily to avoid emotions

- Take help from us whenever required and have faith in long Term Investing

To have a personalized investment plan on long-term investing strategies, please feel free to reach out.

Regards,

**GYC by Dinesh Aneja

+91 8800203200**

Read More →

Category

Personal Finance

**1. Goal is due / Target return is achieved** – There are investments which we make keeping a goal in mind (mostly in mutual fund or in bouquet of products). Such investments are ideally to be reviewed and monitored regularly and often get moved to less volatile products as the goal year is coming nearby. Then there are investments which are made keeping a target return in mind (mostly from investments in stocks). Exiting from all these planned investments should be a no-brainer provided you do not get greedy or fearful during such time.

**2. Non-performance / Change in strategy** – Such decisions often come out of a review meeting where your portfolio is analysed in detail. If certain investments in your portfolio have been consistently lagging in performance compared to peer group of products – then it could be the right time to exit and switch to some better alternatives. Or there may be a change in fund objective or strategy which is not fitting your requirements – then also exiting could be an option.

**3. Financial emergency** – Despite having a sizeable amount in emergency or contingency fund – there could be scenarios, where taking money out of the investments is the only option - we are left with. In such situations, though considering market level or outlook is secondary – but it is of primary importance to consider – which investment to part with. Consider the potential gain you are sacrificing, tax impact, exit load etc. before finalizing on which product to exit from.

Any time is good time to invest – this sentence has almost become a common parlance for all investors like us and largely for long-term investors – this is true also. But not many are talking about right time to take our money out of investments. Whether you consider redemption as a part of personal finance strategies or as a need – it makes lot of sense to know a thing or two about redemption.

Read More →

Category

Personal Finance

**Risk appetite** is how much risk an investor is ready / willing to take. On basis of his answer, we often mark him as an aggressive, moderate, or conservative investor. Based on only this criterion, if financial products are chosen – chances of going wrong is high. Why? Because such answers, given by investor, largely depends on – current market outlook, investor’s experience with some or other investment products, and finally, herd mentality that exists in that period. None of these are ideal or reliable ways to measure one’s risk profile. Even if we agree that investor is giving genuine, unbiased, and informed answers to risk profile questionnaire – still this may not lead to ideal and optimized investment decisions. What is the alternative then? The answer is – Risk Capacity.

**Risk capacity** of an investor is determined based on – individual financial net-worth, age, income level and above all the time horizon of the planned investment. Trusting risk capacity over risk appetite while finalizing on investment products – is often considered a better choice. Let us understand this with an example of cricket.

**Example 1:** Suppose, Team A, batting first, scored 199 runs in a 50 over match. Now, while Team B is coming to bat second – they can afford to not take any risk and keep a run rate of 4 per over should be sufficient. Here, even if Team B’s risk appetite is high, it makes sense to take a conservative or moderate approach to win the game (or achieve the goal).

**Example 2:** Suppose, Team A, batting first, scored 399 runs in a 50 over match. Now, while Team B is coming to bat second – they cannot afford to go slow as they must maintain a run rate of at least 8 per over. Here, even if Team B’s risk appetite is low, it makes sense to take an aggressive approach to win the game (or achieve the goal).

Relating this to personal finance, suppose a young investor of 30 years age (with not much of net-worth and surplus) is planning to achieve a long-term goal like retirement – choosing only low-yield fixed income assets for the same, will not be recommended – even if he is having a conservative risk appetite. Instead, he should take calculative exposure in well-managed equity assets as the goal is long-term and available surplus is not sufficient.

On the other hand, when the same young investor is planning to achieve a short-term goal like making a down-payment to purchase a house – choosing equity assets for the same will be a strict no-no. Instead, he should consider a non-volatile fixed-income instrument for the same.

The purpose of making investment may differ – going to an expensive vacation, foreclosing an outstanding loan, funding for children’s higher education or securing own retirement years etc. But while implementing any of these investment decisions – we must pick and choose some or other financial products. At this juncture knowing investor’s risk profile is said to be of paramount importance, which consists of his/her risk appetite and risk capacity. What is what? Let’s check. Read on.

Read More →

Category

Personal Finance

First things first – gold itself should not be considered as an asset class, the right asset class in this regard could be ‘commodity’ as a whole. But the awareness and availability of other forms of commodity is still very rare and sparse. So, in that case if we consider gold itself as an asset class, then how it is placed against all other asset classes (e.g. equity, debt, real estate etc.)?

➜ Still in our country, gold is largely bought and kept in physical form and mostly in form of jewellery. It is somehow considered as holy, a part of social custom, an ideal gift on some occasions and above all – a status symbol. In all these cases, gold actually turns out to be a dead asset, as it is never sold neither it results in any sort of income stream. If you ignore the notional value of it and consider the cost of maintaining a locker to keep your physical gold safe, it even results in negative return.

➜ Off late, people started buying gold in digital form, where gold as a unit gets credited in your demat account like shares and bonds. Here, your holding reflects the gold price. So, when you decide to trade, equivalent amount of money gets credited in your bank account. With that money, you can then buy physical gold or spend in whatever way you want.

➜ Sovereign Gold Bond (SGB) tries to address this issue by giving you a regular income stream at the rate of 2.50% (taxable) p.a. payable half- yearly. If you hold the SGB till its maturity i.e. 8 years, then post maturity you need not pay any capital gain tax. After 5th year, you can sell it back to government on the date of interest payout. Anytime you sell it whether back to issuer or to a buyer (as it is tradable in exchange) after 3rd year and before maturity – you end up paying long term capital gain @ 20% with indexation (i.e. inflation factored in). Selling it before 3 years will attract short term capital gain tax as per your tax bracket.

Now the question is – should gold be part of your investment portfolio? The answer is – need not be in case of long-term goal-based investing. If your investment horizon is long term and you are overall bullish about India growth story and economy – you can very well keep predominantly equity and some percentages of debt asset.

If your investment horizon is medium term or short term and you are worried about economic downturn, rapid rise of inflation, Indian currency losing purchasing power – then you can very well consider gold as part of your investment portfolio.

But if your purpose is diversifying your portfolio to generate certain benchmark return, keeping 5 – 10% of gold asset in portfolio often proved out to be a good strategy. Of course, in such cases gold must be bought/kept in paper or digital form. Multi-Asset Allocation Mutual Fund schemes also offer a readymade solution in this regard and can be considered.

Should Gold be part of your investment portfolio? If yes, then how much? In that case, in what form should we buy gold – physical gold jewellery, bars, coin, Gold ETF or SGB (Sovereign Gold Bond)? Questions are many. As usual, in many other cases of personal finance, here also the answer is – “It depends”. But it depends on what and how much? Let’s discuss.

Read More →

Category

Personal Finance

**Deciding on Financial Roadmap** – This includes fixing a financial goal with definite time-period, target, and priority. This may sound simple but requires serious time and effort. Very few people do it with sincerity. This is either done in half-hearted casual manner or never done it at all. This exercise often gets postponed for ever. For example, finding out the current cost of education to plan for child’s higher education goal, is often not done properly. Even if the goals are fixed and planned, implementation of the same are often not done immediately or required investment amounts are compromised.

**Related Actions (e.g. review / documentation / technology)** – This is by far the most ignored area of managing personal finance by many. People rarely sit for a review session with their advisors in time. Also, the outcome of review is rarely followed by many. Still many investors do not include their family members in this journey. Documenting all investments and insurance in one place, is again an ignored area of action. Getting acquainted with latest technology, following its safety guidelines and best practices, are also overlooked unfortunately.

**Behavioural Finance** – In books or in insights shared by famous investors, it is frequently mentioned, that real wealth is created through long-term regular investing – but very few of us rarely practice this (unless we forget about an investment!). Though we are not supposed to compare the returns generated by our portfolio with others – still many of us do that and feel good or bad about this. Coming out of an investment is equally difficult for many of us – as either we feel greedy or egoistical about it.

The more seriously we follow the sermons of great investors – the better for us and our family. Let’s give it a try, once more. Never say never. All the best!

Like in every aspect of life, we behave quite differently in managing our finance than mentioned in books and in theories. Of course, those books are written for our benefits and those theories are formulated for our financial wellbeing, but still, most of us rarely could follow such guidelines ditto in our everyday life. How funny or contradictory it may sound, but it is the reality. Let’s discuss few such areas of personal finance where theories and practical implementations differ a lot. Again, such things cannot be said in general, as there are exceptions, but still such a discussion may hit us when we will tend to divert again, if ever, from the theory.

Read More →

Category

Personal Finance

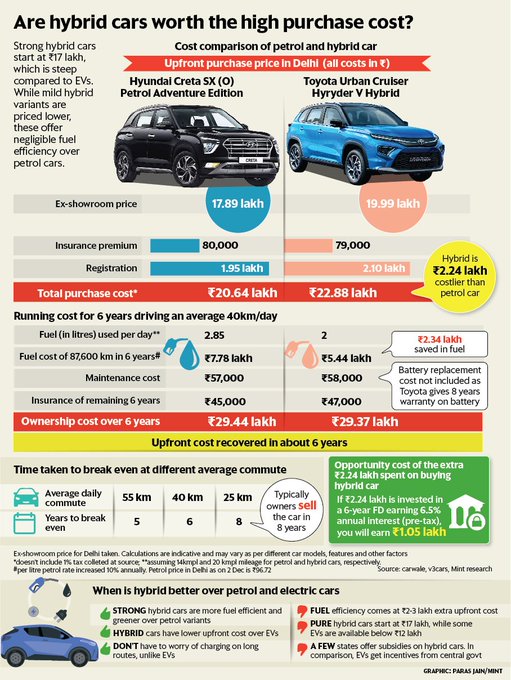

**Should you buy a hybrid car in India?**

Probably, no. The fuel saving doesn't offset the upfront cost by a big margin. Especially if you don't drive much. EVs are also cheaper. This article is an example of how one should assess everthing before buying any asset, doing large expenses or investing as well. Every penny saved would lead you to better days ahead !

Source: https://www.livemint.com/

Read More →

Category

Personal Finance

Three pertinent questions in anyone’s personal finance can be these – how much life insurance cover I require – how much corpus should I target to accumulate so that my retirement years are spent without any financial stress – how can I achieve ‘financial freedom’ even before my retirement year?

What if I tell you that the answers to all these three questions are closely interconnected and can be found out using exactly the same formula? Not believing me? Let’s check.

Say, you are aged 40, planning to retire at age 60 and assumed life expectancy is 85 years of age. Also, your current monthly household and lifestyle expenses stand at 50,000 per month. Other assumptions include – 7% inflation and 10% average return from post-retirement portfolio of investments. Considering all this, you will then need to have a retirement corpus of Rs. 3.62 Crore at your age 60.

Now, suppose you wish you had enough money to retire tomorrow morning. That is, your assumed retirement age is also 40. Then you would be requiring Rs. 1.47 Crore for that to happen, which is nothing but your ticket to ‘financial freedom’ - in other words you would no longer needs to work for money anymore. Financial freedom need not be planned immediately though, you can aim to achieve financial freedom even after a few years also.

So far, we have only considered planned or voluntary retirement. What if, a family’s breadwinner’s income stops because of his/her untimely demise. The required amount is still the same i.e., the amount he/she requires for immediate financial freedom. Or we can call this amount now – the required amount of ‘life insurance cover’ that one must have.

I hope, by now, you are fully convinced that – retirement corpus, financial freedom amount and required amount of life insurance cover – are all closely interconnected.

Read More →