Recent Blog

Category

Taxation

**💡 HUF & Tax Saving Explained**

A Hindu Undivided Family (HUF) is a powerful and fully legal tax-saving structure under Indian income tax law. It helps in income splitting and long-term wealth management by treating the family as a separate taxable entity.

**🔑 Key Highlights:**

• HUF is treated as a separate “person” from its members for tax purposes.

• Income can be legally split between individual members and the HUF, reducing overall tax liability.

• HUF can claim deductions under Section 80C, 80D, and capital gains exemptions, just like an individual.

• Enjoys a separate basic exemption limit:

– ₹2.5 lakh under the Old Tax Regime

– ₹4 lakh under the New Tax Regime

**📌 What is an HUF?**

HUF stands for Hindu Undivided Family. It is a separate legal entity recognized under the Income Tax Act, created specifically for tax purposes.

An HUF is one of the most effective and fully legal tax-saving structures available to joint families.

An HUF can:

• Own property

• Earn income

• Make investments

• Claim tax benefits independently of its members

This helps families reduce their overall tax liability by legally splitting income between individuals and the HUF.

The head of the HUF is called the Karta, and the family members are known as coparceners.

**👨👩👧👦 Who Can Form an HUF?**

• Hindu, Buddhist, Sikh, and Jain families are all eligible to form an HUF.

• An HUF cannot be created by a single person — a minimum of two members is required.

• There must be a family with lineal ascendants and descendants.

• An HUF can also come into existence upon marriage.

**👥 Who Are the Members of an HUF?**

An HUF consists of a common ancestor and all lineal descendants, including their wives and unmarried daughters.

🔹 *Karta*

• The head of the HUF, usually the senior-most male or female member.

• Manages the HUF’s financial and legal affairs.

• Has unlimited liability, including for tax obligations.

🔹 *Coparceners*

• All male and female lineal descendants of the common ancestor.

• Daughters are coparceners by birth with equal rights.

• Have the right to demand partition of HUF property.

🔹 *Other Members*

• Wives of coparceners become members after marriage.

• They are not coparceners.

• Have maintenance rights but cannot demand partition.

**📌 Important Note:**

Only coparceners can seek partition of an HUF, while the Karta bears unlimited liability for HUF dues, including taxes.

**🧾 How to Form an HUF – Step-by-Step Guide**

Forming a Hindu Undivided Family (HUF) is a simple and legal process. It mainly involves creating an HUF deed, obtaining a PAN, opening a bank account, and starting HUF operations.

✅*Step 1: Create an HUF Deed*

The first step is to draft an HUF deed.

The deed should include:

• Name of the Karta

• Names of coparceners/members

• Personal details of all members

• Date of formation of HUF

• Initial HUF corpus and its source

• Any other relevant declarations, as required

📌 This deed acts as the foundation document of the HUF.

✅ *Step 2: Obtain a PAN Card for HUF*

• Apply online for a separate PAN card in the name of the HUF.

• The Karta applies using Form 49A along with necessary declarations.

• In most cases, the PAN number (digital PAN) is generated within 48 hours.

✅ *Step 3: Open an HUF Bank Account*

• Once the PAN is issued, open a bank account in the name of the HUF.

• All HUF income and expenses should be routed through this account.

• Documents generally required:

– HUF Deed

– HUF PAN

– Karta’s PAN & KYC documents

✅ *Step 4: Transfer Common Assets to HUF*

• Assets meant for HUF use—such as property, cash, deposits, or investments—can be transferred to the common HUF pool.

• These assets will then generate income taxable in the hands of the HUF.

[image]how-to-create-huf.jpg[/image]

**📊 Tax Implications of HUF**

*🏠 HUF Residential Status*

The residential status of a Hindu Undivided Family (HUF) depends on where its control and management are exercised during the financial year.

*✅ Resident HUF*

An HUF is considered Resident in India if:

• Its control and management are wholly or partly in India during the previous year.

*📌 Partial control in India is sufficient to treat the HUF as resident.*

Based on Karta’s status:

• If the Karta is Resident and Ordinarily Resident (ROR) → HUF is ROR

• If the Karta is Resident but Not Ordinarily Resident (RNOR) → HUF is RNOR

*❌ Non-Resident HUF*

An HUF is treated as Non-Resident if:

• Its control and management are wholly outside India during the previous year.

🔎 Bottom Line

The residential status of an HUF is primarily linked to the residential status of the Karta, only when the HUF is controlled or managed from India.

If the control and management are outside India, the HUF will be treated as Non-Resident, regardless of other factors.

**💰 HUF Tax Slabs**

• HUF taxation is similar to individual taxation, with minor differences.

• Tax slabs for HUF are the same as for individuals under both:

– Old Tax Regime

– New Tax Regime

📌 The tax slabs remain the same whether the HUF is Resident or Non-Resident, under both regimes.

**New Tax Regime Slabs**

Under the new regime, the tax slabs of HUF for the financial year 2025-26 are as follows:

[image]blog-i/huf-slabs-new.jpg[/image]

**Old Tax Regime Slabs**

[image]huf-slabs-old.jpg[/image]

📌 Note:

👴👵 Relaxed slab rates available for resident senior & super senior citizens are ❌ not applicable to HUF.

💰 Surcharge and cess will be applicable as per prevailing rates.

**🔔 Rebate – Important Clarification**

❌ It is a common misconception that HUFs can claim rebate if taxable income is:

• below ₹7 lakh (New Regime)

• below ₹5 lakh (Old Regime)

• below ₹12 lakh (New Regime for FY 2025-26)

👉 Reality:

🚫 Rebate is NOT available to HUFs.

✅ Rebate can be claimed only by Resident Individuals, not HUFs.

*🏛️ HUF Tax Benefits (Still Powerful!)*

✅ HUF is treated as a separate taxable person, different from its members.

✅ Hence, separate tax slabs & deduction limits apply.

📊 Income can be legitimately split between members and HUF, helping reduce overall family tax liability.

*Basic Exemption Limit:*

• 🧾 Old Regime: ₹2.5 lakh

• 🧾 New Regime (FY 2025-26): ₹4 lakh

***💡 Key Tax Benefits Available to HUF***

🔹 Section 80C – Deduction up to ₹1.5 lakh

👉 PPF, ELSS, Life Insurance, etc.

🔹 Section 80D –

🏥 Deduction on health insurance premium paid for HUF members

🔹 Section 80G –

❤️ Deduction on eligible donations made by HUF

🔹 Home Loan Benefits –

🏠 Deduction on interest paid on housing loan

🔹 Capital Gains Exemptions –

📈 Relief under Sections 54, 54F & 54EC on reinvestment of long-term capital gains

**🏛️ How to Save Taxes by Forming an HUF?**

Let’s understand HUF taxation with a simple example 👇

👨💼 Case Study

👤 Mr. Rajesh Sharma forms an HUF with:

👩 Wife | 👦 Son | 👧 Daughter

🏠 A property owned by Mr. Sharma is transferred to the HUF, earning:

➡️ Annual Rental Income: ₹15 lakh

💼 Mr. Sharma’s Salary Income (individual): ₹20 lakh

📊 Tax Impact – New Tax Regime (FY 2025–26)

🔹 Without HUF (Only Individual Income)

👉 Total Income = ₹35 lakh

💸 Entire income taxed in Mr. Sharma’s hands

➡️ Higher slab = Higher tax outgo

🔹 With HUF Structure (Smart Planning)

🧍 Mr. Sharma (Individual):

💼 Salary Income = ₹20 lakh

🏛️ HUF (Separate Tax Entity):

🏠 Rental Income = ₹15 lakh

👉 Income is now split between two PANs ✔️

👉 Separate basic exemption for HUF applies ✔️

👉 Lower effective tax slabs ✔️

[image]huf-vs-salary.jpg[/image]

**📊 Tax Comparison: With vs Without HUF (New Regime – FY 2025–26)**

[image]tax-comparison.jpg[/image]

**⚠️ Risks & Challenges of an HUF**

While an HUF is an effective tax-saving tool, it also comes with certain limitations 👇

❌ Key Disadvantages of Forming an HUF

🔹 Partition Disputes

👨👩👧👦 Differences among family members can lead to legal and emotional conflicts.

🔹 Complex Compliance

📑 Separate PAN, ITR filing, accounting & documentation increase compliance burden.

🔹 Limited Applicability

⚖️ Benefits apply only in specific income scenarios (rent, capital gains, investments).

🔹 HUF Cannot Receive Salary

🚫 Salary income cannot be routed through HUF — it must be earned by individuals only.

🔹 Dissolution is Not Easy

🔒 Once created, exiting an HUF can be complicated.

**🏛️ Dissolution of an HUF (Partition)**

An HUF can be dissolved only through partition, where assets are distributed among coparceners (members with inheritance rights).

🔸 Types of Partition:

✅ Total Partition

📦 All HUF assets are divided

🚫 HUF ceases to exist

✅ Partial Partition

📦 Only some assets are divided

🔄 HUF continues with remaining assets

📜 Legal Requirements for Valid Partition

📝 Partition Deed must be:

✔️ Drafted

✔️ Properly stamped

✔️ Registered

🪪 HUF PAN Card

➡️ Must be surrendered to tax authorities after total partition

📌 Bottom Line:

🧠 HUF is powerful for tax planning

⚠️ But needs family harmony, long-term vision & professional structuring

A Hindu Undivided Family (HUF) is a separate legal and tax entity under Indian income tax laws, consisting of a common ancestor and lineal descendants. An HUF has its own PAN, tax slabs, and deduction limits, enabling legal income splitting and tax optimisation. It can earn income from assets, investments, and capital gains, though salary income cannot be routed through an HUF.

**📌 Disclaimer: This information is for general awareness only. Tax treatment may vary based on individual circumstances—please consult your Chartered Accountant (CA) or tax advisor for detailed and personalised advice.**

Read More →

Category

Mutual Fund

**🌟 The Shine of Silver — 100%+ Gains in 2 Years**

It’s been a dream run for metal investors.

In India, silver has doubled from around ₹70,000/kg to ₹1.45 lakh/kg in just one and half years — rewarding patient investors handsomely.

Gold too has performed well, but silver clearly stole the spotlight in this cycle as expected.

Lately, I’ve been flooded with questions from clients and investors asking — “Silver has doubled in 2 years! Should we book profits or hold on?”

**Here’s my short and clear view 👇**

**⚙️ Why Silver Rallied So Strongly**

✅ Growing industrial demand from solar, EVs & electronics

✅ Tight global supply and low inventory levels

✅ Inflation hedge appeal in uncertain times

✅ Central banks & retail investors adding to demand

**💡 What Should Investors Do Now?**

If you’ve been holding silver and sitting on big gains, it’s time for a strategy check — not panic, not greed.

🔹 1. Book Partial Profits

Lock in 25–40% of your gains.

Secure profits without fully exiting — always better to book smartly than chase peaks.

🔹 2. Diversify Your Portfolio

Shift a portion into gold ETFs or equity mutual funds.

Gold adds stability, equities drive growth. Balance matters more than timing.

🔹 3. Keep a Core Silver Position

Don’t exit completely — industrial and green-energy demand may keep silver buoyant over the next few years.

🔹 4. Watch the Tax Angle

If you’ve held silver for over 3 years, you qualify for 20% long-term capital gains (LTCG) with indexation benefits.

Plan exits accordingly to save tax.

🔹 5. Stay Disciplined

Silver is volatile. Avoid emotional trades and keep portfolio exposure moderate.

Also, Silver has a long history of thrilling investors—and testing their nerves.

**2011 Peak:** Silver skyrocketed from ~$30 to nearly $49/oz in just a few months. Headlines screamed “Silver to $100!” Investor euphoria was at its peak. Retail investors poured in, driven by fear of missing out. But the bubble burst sharply—silver fell back below $30 in the following year.

**2020–2025 Rally:** After years of sideways movement, silver rallied from ~$15 to $27–30/oz, doubling for long-term holders. Once again, euphoria gripped markets—calls, messages, and “silver everywhere” sentiment flooded investors’ minds.

🧭 **The Bottom Line**

Silver has rewarded patience — but every strong rally needs rebalancing.

Celebrate the profits, but stay smart:

👉 Book some gains

👉 Diversify across gold and equity

👉 Hold a core position for the next leg of growth

In investing, discipline always shines brighter than metal. ✨

📞 Need Help Rebalancing Your Portfolio?

Let’s make your gains work smarter.

📲 Call/WhatsApp: +91 8800203200

🌐 Visit: www.gycbydineshaneja.in

📸 Follow on Instagram: @gyc_dineshaneja

Read More →

Category

Personal Finance

**💔 In 2025, even the Big 4 — Groww, Zerodha, AngelOne & Upstox — together lost 20 lakh users!**

👉 Just in August, over 7 lakh traders pressed EXIT! 🚪

🎢 Is the F&O Party Slowing Down? 🥂

Retail traders who once rushed into weekly options are now pulling back.

⚡️ High-risk thrills are fading.

⚖️ Regulations are tightening.

💸 Quick-money dreams → turning into losses.

**🏛 What Policymakers Did:**

🔺 Higher Margins → More capital needed.

📉 Less Expiries → Fewer thrill rides every week.

🚧 Entry Barriers Raised → Small traders squeezed out.

💰 Higher Taxes → Eating into short-term profits.

**📊 My Client Story**

👉 From my own experience as an MFD (Mutual Fund Distributor) — I’ve seen this shift first-hand.

📌 50% of the clients I onboarded this financial year came from discount brokers!

But when markets turned choppy, many realized that DIY trading isn’t always wealth creation.

That’s when they leaned on me for guidance:

🤝 Hand-holding in volatile times.

🛡 Helping control fear & greed.

📈 Keeping long-term wealth discipline intact.

💡 Showing opportunities beyond just “quick trades.”

**🔄 Where Are They Moving?**

💹 Equity Mutual Funds → Thematic & sectoral bets growing:

PSU 🚂 Infrastructure push.

Healthcare 🏥 Defensive, steady growth.

Consumption 🛒 India’s demand story driving FMCG, retail, lifestyle.

👨💼 PMS → Tailored wealth play for HNIs.

🏦 AIFs → Alternative routes gaining love.

📑 Managed Portfolios → Safer, low-stress investing.

**🌐 The Big Picture**

Retail’s “option trading masti” → slowing down ⏸️

Shift from speculation 🃏 → managed investing 📊

Brokers now eyeing Advisory | Wealth | MF Distribution.

**⏳ Is this a short pause… or a permanent structural shift? Time will tell.**

👤 Dinesh Aneja

📞 +91 8800203200

🌐 www.gycbydineshaneja.in

**💡 Helping you invest wisely, not wildly! 🚀**

Read More →

Category

Mutual Fund

**📈 Investor Note**

**🌾 Agriculture & Trade Dynamics**

🇺🇸 US Interest in Indian Agriculture – The US continues to seek entry into India’s agriculture sector.

🛡️ Policy Safeguards – Strong government policies have limited external access, ensuring protection of domestic interests.

⚠️ External Pressure – Higher tariffs and trade measures are being deployed to create challenges for India’s economy.

**🛍️ Consumption Sector Resilience**

👥 Large Consumer Base – India’s 1.4+ billion population remains a strong driver of demand.

💰 Rising Middle Class – Increasing disposable incomes and expanding middle-class households are fueling steady consumption.

🌾 Agriculture as a Growth Enabler – Rural consumption, supported by agriculture, continues to boost FMCG, retail, and discretionary sectors.

💪 Long-Term Strength – Despite global pressures, India’s domestic consumption-led growth remains resilient and a compelling long-term story.

**💡 Implication for Mutual Fund Investors**

India’s consumption theme continues to be one of the strongest investment opportunities, with agriculture acting as a stabilizing force for rural demand. While external trade challenges may cause near-term volatility, the long-term trajectory of consumption-driven growth makes equity participation—especially in FMCG, retail, consumer discretionary, and rural-focused funds—an attractive proposition for investors.

**📞 Contact for More Insights**

👤 Name: Dinesh Aneja

📧 Email: dineshaneja@gmail.com

🌐 Website: www.gycbydineshaneja.in

📱 Phone: +91 8800203200

📸 Instagram: @gyc_dineshaneja

Read More →

Category

Mutual Fund

**🔍 What is a Mutual Fund?**

A Mutual Fund is a financial vehicle that pools money from multiple investors and invests it in a diversified portfolio of stocks, bonds, gold, and other securities. These funds are professionally managed by Asset Management Companies (AMCs).

📌 You invest.

📌 The fund manager decides where to invest.

📌 You earn returns based on the fund’s performance.

**🧠 Why Should You Consider Mutual Funds?**

✅ Diversification: Spreads your risk across multiple assets

✅ Professional Management: Experts handle your money

✅ Affordability: Start SIPs as low as ₹100/month

✅ Liquidity: Easy to buy/sell, especially in open-ended funds

✅ Transparency: Regular disclosures & regulatory checks by SEBI

**📊 Types of Mutual Funds in India**

[image]mf-type.jpg[/image]

**📈 Realistic Growth – How Much Can You Expect?**

Equity Funds: 12%–18% annually (long-term)

Debt Funds: 5%–8% annually

Hybrid Funds: 8%–12% annually

ELSS: 10%–15% with tax benefits

🕒 Longer horizon = Higher compounding returns

**📊 Mutual Fund Growth Trends (India 2024–2025)**

💰 ₹58 lakh crore+ AUM (Assets Under Management) – July 2025

🚀 Massive inflows in SIPs – ₹20,000+ crore monthly

📈 Surge in midcap, smallcap, and thematic funds

🧑💻 Growing investor base from Tier 2 & Tier 3 cities

**📊 Taxation Summary Table**

[image]tax.jpg[/image]

**🧭 How to Start Your Mutual Fund Journey?**

1️⃣ Define Your Goals

🎯 Retirement, child’s education, dream home, or wealth creation? Start with purpose.

2️⃣ Know Your Risk Appetite

⚖️ Are you conservative, balanced, or aggressive? Your risk level shapes your fund choice.

3️⃣ Choose the Right Fund Type

📈 Short-term = Debt | Medium = Hybrid | Long-term = Equity/ELSS

4️⃣ Start SIP or Lump Sum

💸 Start small with SIPs or go big with lump sum. Automate & stay disciplined.

5️⃣ Track, Don’t React

🔍 Review your funds yearly, not daily. Ignore short-term noise—focus on long-term growth.

**🔑 Pro Tips for New Investors**

🌱 Start Early – Time is your biggest asset

📉 Don't Panic – Markets have short-term noise

🧾 Use SIPs – Rupee cost averaging over time

👩⚖️ Stay Compliant – Complete KYC, track tax rules

📊 Review Annually – Realign based on goals

**🙋 Common Myths Busted**

❌ Mutual funds are only for experts – NO. Anyone can start!

❌ You need lakhs to invest – Start with just ₹100

❌ High returns are guaranteed – Returns are market-linked

**🧑💼 Why Choose a Mutual Fund Distributor like us ?**

✅ Personalized Advice – Funds matched to your goals & risk profile

🧾 Tax Planning Help – ELSS, capital gains & ITR support

📊 Ongoing Portfolio Tracking – Reviews & rebalancing done for you

🧠 Emotional Guidance – Helps avoid panic during market dips

🤝 Human Support – Phone/WhatsApp help, not just apps

We doesn’t just sell funds – we build wealth with you and maintain relations.”

**🎯 Final Thoughts**

Mutual Funds are India’s most trusted and accessible investment option today — for salaried individuals, business owners, and even students. With the power of compounding and strategic planning, you can build wealth, beat inflation, and achieve your financial goals.

**📲 Need help choosing the right fund?**

DM us on Instagram @gyc_dineshaneja or

WhatsApp 📞 +91 8800203200

Read More →

Category

Taxation

Under the Exempt-Exempt-Exempt or EEE scheme, earnings, gains as well as withdrawals are tax-free*. It is a popular tax-saving scheme that helps in long-term financial planning.

Taxes act as fuel for government funding. They are crucial for supporting necessary public services, such as education and healthcare. While paying taxes is the responsibility of every eligible citizen within a country, high taxation can lead to a financial burden on some taxpayers. At this point, concepts like EEE come into play.

Exempt-Exempt-Exempt, or EEE, is an important concept in the taxation system that allows individuals to build wealth and save tax while complying with the regulations. Under this scheme, all investments, earnings and withdrawals remain tax-free.

Simply put, you can grow your savings and earn interest on them without worrying about paying anything to the tax authorities under the EEE scheme of Section 80C.

Let us discuss more about the EEE scheme, including EEE tax regime investment products, in detail.

**What is EEE in Income Tax?**

Exempt-Exempt-Exempt is a tax-exemption scheme that correlates with the deductions under Section 80C of the Income Tax Act. Certain tax-saving instruments can be utilised under this scheme to save tax on investments, interests, and maturity.

***Exempt Investment:*** The initial investment you make towards an EEE-qualified instrument is itself exempt from income tax. This means a portion of your salary saved in these schemes escapes tax deductions, reducing your taxable income. Think of it as putting your money to work without losing a chunk to the taxman!

***Exempt Interest:*** The interest earned on your investment within the EEE scheme also enjoys tax exemption. As your money grows with compounded interest, the accrued gains remain untouched by the tax net. This allows your nest egg to flourish tax-free, accelerating your wealth accumulation.

***Exempt Maturity Proceeds:*** The cherry on top? The final payout – the maturity proceeds you receive upon completion of the investment tenure – is also exempt from income tax. You reap the full rewards of your investment, principal and interest combined, without facing any tax liability.

**Top EEE Investment Options to Consider**

***PPF***

Perhaps the safest and most popular tax-saving scheme that has benefited individuals for decades is the PPF. It is still a highly sought-after investment option among taxpayers due to its risk-free nature.

Backed up by the Central Government, it offers an opportunity to earn tax-free returns. You can open a PPF account in the bank or any local post office or nearest bank.

Note that this scheme has a 15-year initial lock-in period. Once the plan reaches maturity after 15 years, you can extend the tenure in a block of five years. Under Section 80C, PPF offers tax deductions up to ₹1,50,000 per annum but limitation is on the withdrawals.

***Unit Linked Insurance Plans (ULIPs)***

ULIPs**, or Unit Linked Insurance Plans, are known for offering a variety of investment features and benefits. Some of the most attractive features of ULIPs include automatic portfolio management, goal safety, and multi-fund allocation.

In general, most ULIPs offer around 5 to 9 fund options with different asset and equity allocations. Further, they usually come with a lock-in period of five years, but you can extend it up to 20 years, depending on your preferences. Besides Section 80C deductions, ULIPs also offer exemptions on death benefits under Section 10(10 D). Here, the catch is that maximum about invested in ULIP can not exceed 2.5 Lakhs per annum.

***Equity Linked Savings Scheme (ELSS)***

It is another EEE investment option that can be used for saving tax. Note that it allows you to enjoy tax-free capital gains up to ₹1,00,000. However, as your gains exceed ₹1,25,000, you will have to deal with long-term capital gains tax (LTCG) at the rate of 12.5%.

***Sukanya Samriddhi Yojna (SSY)***

Sukanya Samriddhi Yojna was introduced as a part of the “Beti Bachao Beti Padhao” initiative of the government. It aims at assisting the guardian of a female child to raise funds for her future. You can have an SSY account in the name of your girl child, offering an annual interest rate of 7.6%. Note that the maturity amount and the interest earned are tax-free under this scheme.

***Employee Provident Fund (EPF)***

Finally, EPF, or simply PF, is a retirement program that falls under the EEE scheme. In this option, employers and employees are eligible for interest and are not subject to tax implementations under certain conditions. If you withdraw your EPF amount after its maturity, all your contributions, interests and withdrawals remain tax-free.

**Final Thoughts**

Exempt-Exempt-Exempt (EEE) has become a popular tax-saving option among taxpayers. Investing in products under the EEE scheme helps you maximise your earnings and gains while minimising your tax liabilities.

In this blog, we have discussed the top EEE investment options to choose from. Now, it is your turn to make the right choice considering your financial situation, annual income, long-term financial goals, and other deductions under Section 80C.

Our take is to go with ULIP as it gives following benefits:

1. Option to invest in Equity Market/Debt funds where scope of returns is more than tradtional investments. Funds can be choosen basis the risk appetite.

2. Switchs between Equity/Debt funds allowed without paying LTCG which is 12.5% on returns earned or STCG which is @ 20.00%.

3. Flexibility to withdraw full amount after 5 years completion and fulfill your all medium term needs.

4. No hassles of Tax Harvesting as returns are tax free if if annual investment was made not more than 2.5 Lakh per annum.

We hope it helps!

Regards,

GYC by Dinesh Aneja

Read More →

Category

Taxation

The Union Budget 2025 had surprisingly pleasant news for the Indian taxpayers and Investors. More so for the so-called and often-ignored Middle Class of India. And what exactly is the good news?

The Indian Taxpayers opting for New Tax Regime and earning less than Rs 12 lakh will have to pay No Taxes.

**So going forward, there would be Zero (or NIL) tax for those with income of up to Rs 12 lakh in a year under the New Tax Regime & Slabs!**

Let’s see how this works given that even in the new tax regime, the tax slabs start from Rs 4 lakh. So many are getting confused as to how the Rs 12 lakh income becomes tax-free when slabs start at a lower income threshold.

It is here that Tax Rebate Under Section 87A comes into the picture.

Here is a simple example to show the working:

**How Income Tax is Zero (NIL) on Rs 12 lakh income under New Regime (2025)?**

Suppose, your net taxable income is Rs 12 lakh.

As per the latest new tax slabs, the calculated normal tax liability is as follows:

0 to Rs 4 lakh – 0% – Nil

Rs 4 lakh to Rs 8 lakh – 5% of Rs 4 lakh – Rs 20,000

Rs 8 lakh to Rs 12 lakh – 10% of Rs 4 lakh – Rs 40,000

So the total tax = 0 + Rs 20,000 + Rs 40,000 = Rs 60,000

But, the revised Section 87A limit now offers a full rebate for taxable income of up to Rs 12 lakh under the new tax regime. Earlier, eligibility for tax rebate under Section 87A was Rs 7 lakh. Now it has been enhanced in Budget 2025 to Rs 12 lakh.

Result?

Tax of Rs 60,000 – Rebate of Rs 60,000 = Zero Tax

So you can say that the so-called zero tax is applicable only for those whose taxable income is Rs 12 lakh or less under the new tax regime.

But what happens in case taxable income is more than Rs 12 lakh?

Let’s see…

**Income Tax on income above Rs 12 lakh in New Tax Regime (2025)**

If you wish to calculate income tax on your net taxable income above Rs 12 lakh, then let’s take an example to understand it.

Suppose, your total income is Rs 14 lakh.

As per the tax slabs, the calculated normal tax liability is as follows:

0 to Rs 4 lakh – 0% – Nil

Rs 4 lakh to Rs 8 lakh – 5% of Rs 4 lakh – Rs 20,000

Rs 8 lakh to Rs 12 lakh – 10% of Rs 4 lakh – Rs 40,000

Rs 12 lakh to Rs 14 lakh – 15% of Rs 2 lakh – Rs 30,000

The total income tax in this case would be = 0 + Rs 20,000 + Rs 40,000 + Rs 30,000 = Rs 90,000

You may ask why aren’t you getting the Rebate under Section 87A in this case.

This is because the revised Section 87A limit is applicable for the new regime only for those who earn less than Rs 12 lakh. And in our example, that limit is crossed as the income is more than Rs 12 lakh.

Since your taxable income is Rs 14 lakh, which is not less than Rs 12 lakh in the new regime, you are not eligible for the rebate under Section 87A of the Income Tax Act.

So your tax liability remains at Rs 90,000 and you have to pay the full amount. Sorry! But you can still be wise about tax planning by **giving priority to your investment planning.**

It makes sense to repeat that the Section 87A Rebate in the new regime is available only if taxable income is Rs 12 lakh or less. Not if it’s above it.

**A few more aspects to remember:**

This increased Rs 12 lakh threshold is for total TAXABLE income, i.e. after considering all deductions that are applicable under the new regime like standard deduction (Rs 75,000), etc. So, if you are a salaried individual, and you get a standard deduction of Rs 75,000, then in your case, a total income of up to Rs 12.75 lakh will be tax-free!

The Rebate under Section 87A is not available for Capital gains. So you can’t adjust it against your taxes on capital gains. Let’s say you earn Rs 6 lakh from salary income and you have another Rs 3 lakh in capital gains. Then even though total earnings are Rs 9 lakh which is less than Rs 12 lakh, the rebate of Section 87A is not applicable on capital gains and hence, you will have to pay capital gains tax on the Rs 3 lakh capital gains (though salary of Rs 6 lakh remains tax-free).

I hope this article clarifies your doubts about how the income of Rs 12 lakh is tax-free under the new tax regime and what is the zero per cent (0%) income tax slab for those earning less than Rs 12 lakh.

**That said, let me remind (and caution) you that while the income of Rs 12 lakh is now tax-free, and hence, there is no theoretical need to save tax, let this not deter you from saving/investing. Paying no tax is good. But you still have to save for the future. Earlier, there was a tax-linked incentive to do so for many. Now, it is up to you.**

Regards,

GYC by Dinesh Aneja

Read More →

Category

Personal Finance

**Responsible Investing:**

The Pain in Mid- and Small-Caps Has Just Begun

Hello everyone,

As we step into 2025, I want to share some insights that are rooted in conversations with fund managers over training session, my own research, and interactions with many of you.

Responsible investing—a subject more relevant than ever given what we’re seeing in mid and small cap stocks.

Over the last few months, almost every fund manager I’ve spoken to has shared a bearish outlook on mid and small caps. Our independent research pointed to the same basis data collated at our end with backtesting results of last 5 years and Macros of the economy. This lead to the same conclusion, leading us to communicate caution and a reduction in exposure (Covered in Sept'24 Blog)

In my last quarter messages, I reiterated this. Yet many clients remain unfazed When Confidence Peaks, Caution Is Key.

This week, I met with an 60-plus-year-old client—a seasoned investor.

For months, I’ve been urging him to reduce his mid-small-cap exposure. Despite my warnings, he remains steadfast, armed with rationale after rationale for why this segment will perform well. His belief is unwavering, driven by a long-term view and recent market performance.

But let’s pause and reflect.

•When seasoned fund managers are nervous, why are individual investors super confident?

•Why do professional risk models flash red while retail investors see green lights?

•Why do they believe in TV stories and Fin influencers and not their own advisors/distributors?

**The Behavioral Trap:**

Recency Bias and Overconfidence

In investing, confidence often peaks just before trouble begins. The last few months felt like a vindication of retail investors’ decisions, as mid- and small-caps continued to rise. However, this false sense of security can blind us to looming risks.

Remember:

•Recency bias makes us believe that what worked recently will continue to work.

•Long-term investing doesn’t mean holding risky assets through a drawdown when market cycles clearly shift.

It’s true that small- and mid-cap companies have immense potential. But every investment must be viewed through the lens of valuation, market sentiment, and macroeconomic reality. Today, those signals suggest that the pain in mid- and small-caps has only just begun.

**What Responsible Investing Means Today**

1.Avoid chasing past winners:

Just because mid- and small-caps have done well doesn’t mean they’ll keep doing so.

2.Balance your portfolio: Diversification into large-cap and multi-cap strategies provides stability along with Debt Funds or hybrid funds.

3.Listen to professional guidance: Fund managers use data and experience to assess risks that aren’t always obvious.

Remember:

Volatility is temporary, but permanent loss of capital can derail your financial goals.

**Conclusion:**

Responsible investing is about managing risk as much as seeking returns. We believe this is a time to stay disciplined and follow a research-backed strategy, even if it feels counterintuitive. While short-term gains may tempt us to hold onto mid- and small-caps, the best investment decisions are often the hardest to make

If you’re feeling unsure about your portfolio exposure, we’re here to help. Let’s work together to ensure your investments align with your goals and today’s market realities.

Stay safe, stay diversified, and invest responsibly to garner the gains of India's long term Growth Story.

Regards,

GYC by Dinesh Aneja

+91 8800 203200

Read More →

Category

Mutual Fund

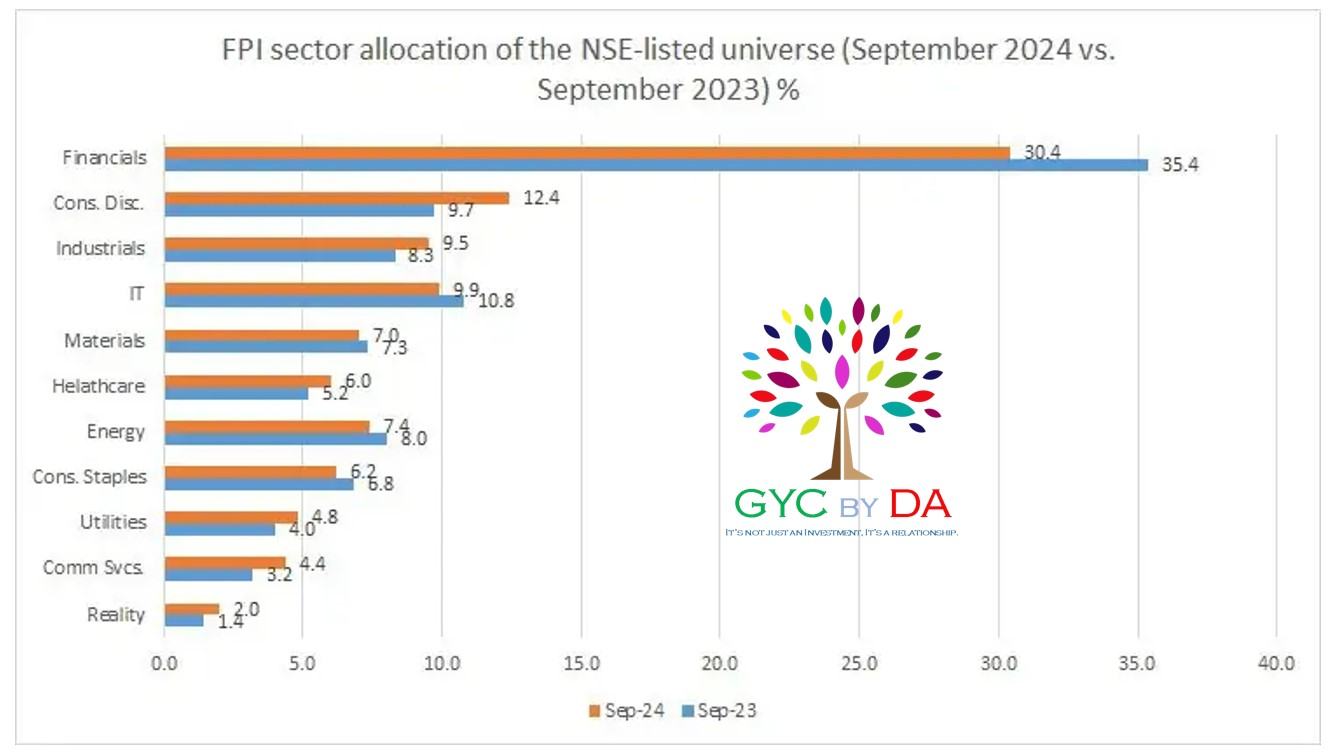

**Foreign Portfolio Investors Reshuffling Sector Allocations in Indian Markets**

Recently, there has been a noticeable shift in the investment strategies of Foreign Portfolio Investors (FPIs) in the Indian stock market. While many are aware that FPIs have been selling, it is important to understand that this is not a simple sell-off. Instead, there is also a significant restructuring of their investments across different sectors. This change highlights a deeper trend in how global investors are adjusting their portfolios to align with market conditions.

**Decline in Financial Sector Allocations**

One of the most significant changes has been in the financial sector, which includes banks and financial services companies. Over the past year, FPIs have reduced their allocations to this sector. The allocation has dropped from 35% in September 2023 to 30.4% in September 2024. This decline represents nearly a 20% reduction in their investment in financials. The financial sector, which once attracted a large portion of FPI funds, is now seeing a shift away as investors look for more stable or growth-driven opportunities.

**Rising Interest in Consumer Discretionary and Industrials**

On the other hand, the consumer discretionary sector has seen a significant increase in FPI investments. The allocation to this sector has risen from 9.7% to 12.4%, marking a nearly 20% jump in just one year. This sector includes businesses related to goods and services that people buy with discretionary income, such as automobiles, entertainment, and luxury products. Similarly, the industrials sector has also seen a rise in allocation, growing from 8.3% to 9.5%. These shifts indicate that FPIs are becoming more interested in sectors that show potential for stable growth, especially in the post-pandemic world.

**Decline in IT and Energy Sectors**

Another noteworthy change is the reduced allocation in the Information Technology (IT) and energy sectors. The IT sector, which has traditionally been a strong performer, saw its allocation drop from 10.8% to 9.9%. This reduction shows that while IT still remains a significant part of FPI portfolios, investors are becoming more cautious about its future growth potential. Energy also witnessed a drop, reflecting changing global market dynamics and perhaps a shift towards more sustainable and diversified investment opportunities.

**Healthcare and Utilities Gaining Attention**

FPIs have increased their focus on more defensive sectors like healthcare, which saw an increase in allocation from 5.2% to 6%. This suggests that investors are looking for safer bets amid market volatility. Utilities, which provide essential services like electricity and water, have also seen a rise in FPI investments. These sectors are known for their stability, especially during economic downturns, making them attractive to investors who seek lower risk.

**Sector Rotation Instead of Mass Exit**

The changes in sector allocations reveal that FPIs are not simply exiting the Indian market. Instead, they are rotating their investments across different sectors. While there may be a net outflow of funds, the allocation adjustments show a strategic approach. FPIs are moving away from sectors that may be considered overvalued or have reached their peak, such as financials, IT, and energy. At the same time, they are increasing their exposure to more defensive and growth-oriented sectors like consumer discretionary, healthcare, and utilities.

Most of the changes are in line with our strategy except Energy Sector where in we've increase our allocation in last few months. It looks good to see that Big Money is following us or we're one step ahead of the FPI :)

Whatever may be reason, but seems that we're on the right path and doing allocation basis the data points recieved in our own system. This gives confidence on our long term wealth creation journey and add values to our clients trust and their portfolios.

Regards,

**GYC by Dinesh Aneja**

+91 88 00 20 3200

Read More →

Category

Mutual Fund

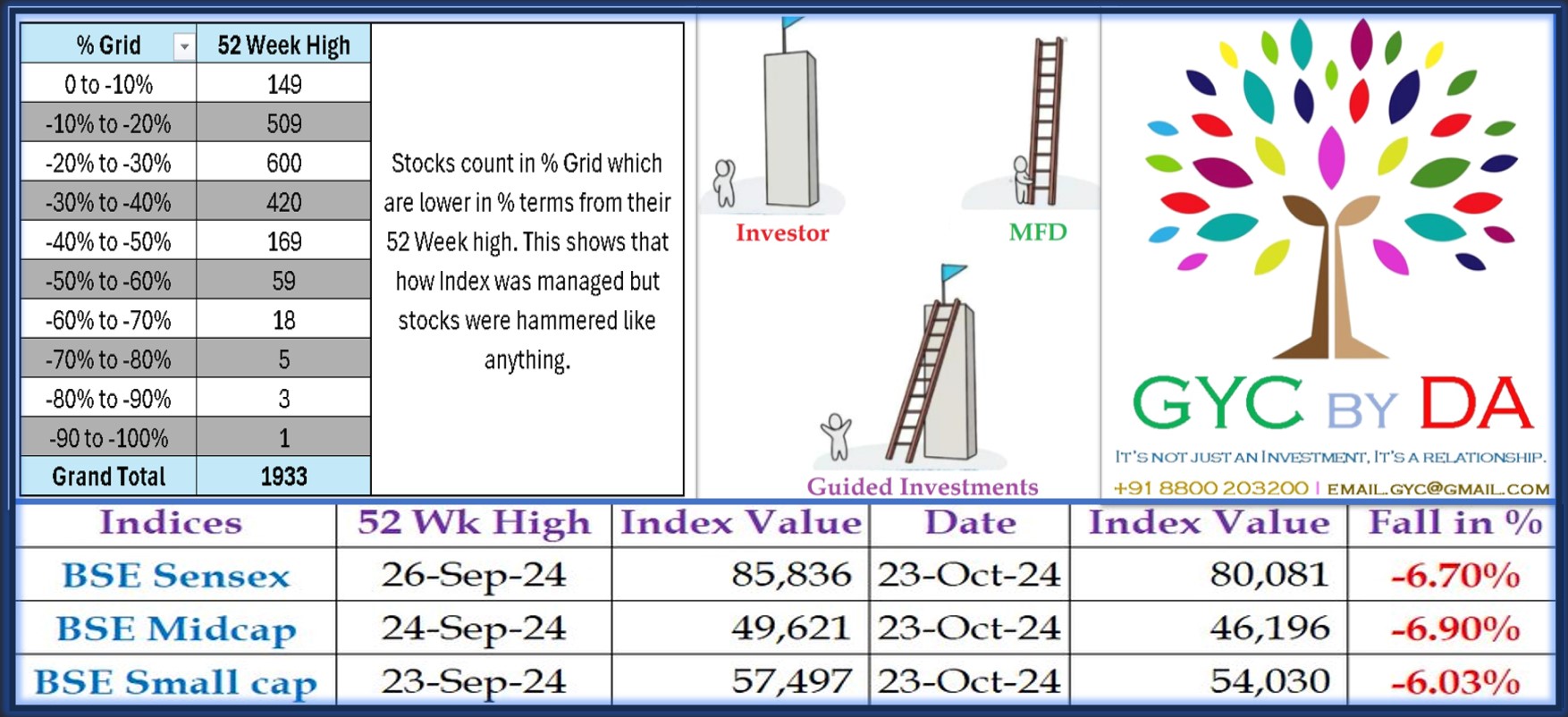

Broader indices are currently down by 7%, causing concerns among many investors. Questions like "What happened to my portfolio?" and "Should I exit now and enter later?" are common during market corrections and I'm getting so many queries now. I had already warned in September and many a times before as well that valuations looks stretched for few sectors specially Mid and Small Cap index. If I talk about the stocks, they have been hammered ruthlessly in last few months. Out of 1900+ stocks listed on NSE India exchange, 70% were down from 10% to 50%. That was the reason that many investors were not able see much growth in their Portfolios which had more concentration of Small and Mid Caps.

Similarly, few sectors run very quikly in last few month but faceing correction now as they got over valued. In Equity Market, chasing returns / sector is very difficult but investors with long term horizon achieve this very easily with proper guidance and research.

However, it's crucial to remember that equity investment is a long-term game. The recent drawdown is just a small draw down of long term wealth creation journey.

Looking back, the Sensex surged from 3,000 to 21,000 between 2003 and 2007, showcasing the market's resilience over time. During the same time market corrected more than 10% on 14 occasions. Market once corrected by 29% and another time by 23% in the same bull run of 5 long years.

**One key piece of suggestion for investors is to avoid checking their portfolios daily. Emotions can lead to reactive decisions that may not align with long-term goals.**

Successful investors understand the importance of staying the course and not being swayed by short-term fluctuations. Patience and a focus on long-term gains are key to navigating the ups and downs of the market.

Regards,

**GYC by Dinesh Aneja

+91 8800203200**

Read More →

Category

Behavioural Finance

Dear Investors,

I've been recieving lots of call now on Equity Market boom and how to increase my allocation in Equity as greed is at its peak. I share my perspectives on a topic, where investors will find useful. This time I delve into value and risk in investing during bull markets.

**A Stock Market Story**

Do you remember the atmosphere in the equity markets towards the end of 2007? The Sensex had been up about five times over the previous five years, and really, there was a madness in the air. There seemed to be no end to how high and how fast stocks could rise. We all remember how it ended, but that’s not my point today. My point is not what happened to the markets when they crashed but to individual companies when they recovered.

Whenever the markets rise like they did then, they eventually crash. It was inevitable then, and it’s inevitable now. There may be some doubt about when it will happen and by how much, but it will definitely happen. But correctly timing of such events is next to impossible. To a seasoned equity investor, this is nothing unexpected. Ups and downs are part of the game as I've seen 2 such major collapse in my life since I started my career in this industry in Jan 2004.

The part that few investors appreciate is that these are dangerous times. Over the next few years, when the dust settles in the next market cycle, you will find that these weren’t great times as far as buying stocks or Equity Mutual fund was concerned. You might think I’m saying this only because during bull runs, valuations are high, and stocks are expensive. You would be right, but that’s not the only reason and the biggest one. The biggest reason is psychological. When anything you buy makes money, the constant scepticism that investors need disappears from their brains.

This euphoria can lead to poor decision-making, where investors ignore fundamental analysis and chase momentum. They may overlook company financial or governance red flags, blinded by the allure of quick gains. Moreover, even mediocre companies can see their stock prices soar during these times, creating a false sense of security. It's crucial to remember that when the tide eventually turns, the quality of the underlying business will determine which stocks survive and thrive, not just market sentiment.

In fact, before the market peaks out, I read a newspaper column with this interesting story: One day, a man appeared in a village and offered to buy all the monkeys that the villagers could supply for Rs 1,000 each. The villagers caught all the monkeys around and sold them. Soon, another man appeared and offered Rs 2,000 for each monkey. However, there weren't any more monkeys around so that the villagers couldn't sell the man anything. However, they figured that, for some reason, the demand for monkeys was going up, so they looked for the first man and bought back all the monkeys for Rs 3,000 each (which was the least the man was willing to take). Unfortunately, this stratagem failed, and the buyer never reappeared, leaving the villagers stuck with the animals.

Nearby, there was another village where the same story was repeated, except it was about goats. The final buyer also never appeared, and the villagers were stuck with the goats. However, there was a big difference. The monkeys were a nuisance. They were noisy, troublesome, and dangerous, and they stole food all the time, so the villagers eventually abandoned them in the forest. The goats, however, were alright. They were easy to keep, grazed on grass and gave milk. When they grew older, the villagers slaughtered them for meat. All in all, buying goats was not the bad deal it looked like initially.

For investors in today’s raging bull market, the moral of the story should be obvious. In this heated market, take great care to differentiate between the 'monkeys' and the 'goats' in your portfolio. The 'monkeys' are the speculative stocks or mutual funds with very high return, hyped up by market sentiment but lacking fundamental value. When the market inevitably corrects, these stocks / funds may prove to be not just worthless but actively detrimental to your financial health. The 'goats', on the other hand, represent companies and mutual funds with with solid fundamentals, strong business models, and the ability to generate real value over time as they can contribute to India's growth story for many years from here on.

The goats are expensive, too, but at least they will deliver value even after buyers disappear. Start looking for goats and sell the monkeys for peace in life as you've already added many species in your Financial Jungle.

The story is sourced from [here](https://www.valueresearchonline.com/stories/10590/monkeys-goats-and-markets/)

Regards,

GYC by Dinesh Aneja

+91 8800 203200

Read More →

Category

Mutual Fund

**The Importance of Sector Selection**

Choosing the right sectors to invest in can make or break your investment strategy. There are years when one sector performs exceptionally well, while others struggle. For example, the automobile sector had a fantastic year in 2014, followed by two relatively bad years in 2015 and 2016. It bounced back in 2017 with an impressive 40% growth but then dipped again in 2018 and 2019 before recovering post-2020. These fluctuations highlight the importance of having a mechanism to exit underperforming sectors while staying invested in sectors that are on the rise.

**The Challenge of Predicting Sector Performance**

It can be incredibly difficult for investors, especially those not following any system or strategy, to predict which sectors will do well. The market is complex, and with ten major sectors to choose from, determining which ones will excel in any given year is a major challenge. Without the help of strategies that automatically select top-performing sectors, investors may find themselves lost in the maze of shifting market trends. This is where the value of structured investment strategies comes into play, offering a systematic approach to sector selection.

**Avoiding Thematic Investments Without a Strategy**

Many investors are tempted to put their money into thematic funds or specific sectors, hoping for a good return. However, this can often lead to long periods of poor performance if the sector they choose does not perform well. For instance, investors who focused on public sector units (PSU) in 2018 and 2019 experienced weak returns during those years. It was only in the last three years that the PSU sector began to recover, rewarding those who stayed invested. Similarly, the pharmaceutical sector had great years in 2014 and 2015, only to suffer four consecutive years of poor performance before bouncing back.

**Embracing a Dynamic Investment Strategy**

The performance of different sectors tends to be cyclical, with new sectoral winners emerging each year. This cyclical nature makes it important for investors to have strategies in place that can adapt to changing market conditions. Momentum strategies, for example, often automatically pick up on sectors that are currently performing well.

So far in last 5 years, we have done very well by rotating the money in Small Cap, Mid Cap, PSU, Infra, Pharma and continue to do well in upcoming sectors of the decade.

Regards,

GYC by Dinesh Aneja

+91 8800 203 200

Read More →

Category

Mutual Fund

Dear Investor,

India’s power sector, shunned by investors for long, is in the spotlight since the pandemic. Economic growth along with technological advancement and electrification threaten a demand surge like never before.

**Govt Policy:**

The National Electricity Plan for central and state transmission systems has projected a total outlay of Rs 9.2 lakh crore. The plan aims to meet a peak demand of 458 gigawatt (GW) by 2032 -- revised higher from the previous estimate of 380 GW. Power sector veterans foresee that power consumption in India will compound by about 7 percent over the next decade.

A detailed report by brokerage and research house MOFS points out that the peak power deficit used to be as high as 15 GW (13 percent of peak demand) in FY2010 and then declined to only 1 GW (or less than 1 percent) during FY19-21. It has been rising over the past two years; in FY23, it surged to 9 GW (4 percent of peak demand).

**Power Consumption and Technology Advancement:**

What’s noteworthy is the shift in power consumption away from core manufacturing industries to new demand drivers such as electric vehicles, data centres and electrification of energy demand. Besides, rising per capita income in India is driving higher household ownership of electrical appliances, too.

Then, there is a powerful price to pay for technological advancement. These technologies such as data centres and artificial intelligence systems that are reckoned to be disruptive, improve efficiencies and cut costs in the long run, are also electricity guzzlers. Ironically, every time consumers around the world undergo a technological upgrade, power demand witnesses a leg-up. For instance, “a simple Google search needs 0.3 Wh of power, while a Chat GPT query consumes 10x the amount of power of a Google search”, according to the Motilal Oswal report.

**Distribution:**

So, with India’s commitment to electrification in mobility and the data centre footprint set to leapfrog, the rising estimates for future power demand appear justified. Details of the NEP indicate significant outlays for transmission systems, storage and distribution and focus on renewable energy and green hydrogen loads into the country's electricity grid.

**What is there for Investors:**

For investors, the much-neglected power sector could turn into a bright long-term opportunity as we informed last week. Some international equity research houses are positive on power asset developers, generators and transmission and distribution companies that are poised to take advantage of the government capital expenditure in this sector. Energy exchanges, too, could gain as expansion of transmission may see new products being launched.

That said, investors must be mindful of uncertain and fluctuating return ratios in the sector, the impact of commodity and component prices on profitability and regulatory risks that have in the past been a stumbling block to private sector investment.

Regards,

GYC by Dinesh Aneja

+91 8800 203 200

Read More →

Category

Personal Finance

From Fear to Fortune: A 10-20 Year Investment Odyssey

In 2008, market turmoil tested your resolve, but wisdom prevailed:

"Don't invest for 10-15%, invest for 10-15 times over 10-15 years. Think like an owner, not a tenant."

Post-35% Fall: A Fresh Start_

**Investment Strategy:**

- Invest ₹10,000/month

- Horizon: 10-20 years

- Asset Allocation: 60-80% Equity, 20-40% Debt

**Projected Growth (CAGR):_**

- 10 years: 12-15% CAGR ( ₹22.5 lakhs - ₹31.5 lakhs)

- 15 years: 15-18% CAGR ( ₹55 lakhs - ₹85 lakhs)

- 20 years: 18-20% CAGR ( ₹1.2 crores - ₹1.8 crores)

**Wealth Creation Milestones:**

- 5 years: ₹8 lakhs - ₹12 lakhs

- 10 years: ₹22.5 lakhs - ₹31.5 lakhs

- 15 years: ₹55 lakhs - ₹85 lakhs

- 20 years: ₹1.2 crores - ₹1.8 crores

**Growth Chart:**

| Year | Investment | Growth |

| --- | --- | --- |

| 5 | ₹6 lakhs | ₹8-12 L |

| 10 | ₹12 lakhs | ₹22.5-31.5 L |

| 15 | ₹18 lakhs | ₹55-85 L |

| 20 | ₹24 lakhs | ₹1.2-1.8 Crs |

**Investment Insights:**

- Consistency triumphs over timing

- Long-term focus beats short-term fears

- Equity investing rewards patience

**Gratitude and Guidance:**

Your mentor's wisdom transformed your investment approach. Now:

- Stay calm amidst market fluctuations

- Focus on wealth creation, not short-term gains

- Embody the owner's mindset, not the tenant's

**Celebrate Your Resilience:**

From fear to fortune, your investment journey has begun anew. Embrace the power of long-term investing.

***Additional Tips:***

- Rebalance portfolio periodically and do the sector rotation from long Term perspective

- Monitor and adjust asset allocation depending upon Macro's

- Stay informed, not emotionally invested

- Don't see your Mutual Fund Portfolio daily to avoid emotions

- Take help from us whenever required and have faith in long Term Investing

To have a personalized investment plan on long-term investing strategies, please feel free to reach out.

Regards,

**GYC by Dinesh Aneja

+91 8800203200**

Read More →

Category

Insurance

**🚨Are online platforms good enough to buy health insurance?**

Consulted a online platform (backed by a leading broker) for buying health insurance as I was having some free time yesterday morning.

On the call I asked them:-

Have my father who is 65 years of age with Diabeties and Hypertension, Which policy will you offer?

They told me they would suggest: HDFC Ergo Optima Secure or Star Health Senior

The person whom I talked to, did not understand my questions in depth as there wasn't any personal connect.

He told me Star is one of the best insurers

When I asked them about the Co-pay / Claims ratio etc. for Star Health and a lot of complaints on social media about the insurer? Agent tried to cook up some unwarranted explanations.

So he suggested to buy HDFC Ergo Optima Secure.

But when I told him the policy doesn't offer day 1 cover for diabetes and hypertension.

So, he said then buy Star Health Senior.

When I asked him about the policy from Care, Manipal Cigna, ICICI, Niva or Aditya Birla, the person did not have in-depth knowledge most any of their policies, In fact I educated him on various other policies.

Health insurance is superbly complex and very few understand the nitty-gritty properly.

You must have an agent who supports you and understands the terms and conditions in depth and provides you the product basis your needs and his/her needs.

Big platforms spend huge money on advertising and social media marketing, but very few of them are unbiased and provide very good advice. They sell what they have been basis their Sales Targets.

*Be very careful while buying policy online and understand the product well to avoid any regret in future. They wouldn't stand with you in case of any claim.

*

In case you still have any doubts, please feel free to reachout to us.

**Regards,

GYC by Dinesh Aneja**

Read More →

Category

Mutual Fund

Good Day Investors!!!

I must confess I have bearish view on midcaps-smallcaps for quite some time now. I never take such calls in haste and I am aware that I am not in business of making predictions but in business of managing risk in my client's portfolios.

Whichever way I slice and dice it my data analysis along with technicals and fundamnentals telling me this is a bubble of epic proportion that will be remembered after long time. We are looking at extremely frustrating phase in coming years. It will be worst for novice traders/investors who want quick money and havn't seen any major downside. The happiest people would be those who do SIP for long term keeping in mind India's growth story intact with Zero loss of emotional capital.

**My call is based on 3 things:**

- Economy is reaching overheated phase and earnings growth will be lower than expected. PE derating + low EPS growth can be killer combination.

- Monetary conditions will remain tight. Rates are cut during recessions not when economy is doing well. Even if are there are odd cuts here and there the liquidity will remain poor. Two other reasons why I don't see big rate cuts are-they hurt savers and lower mortgage rates can create frenzy in real estate crowding out middle class population. I would be surprised if 10Y Gsec dip below 6.5% in next 2 yrs.

- Big ticket purchase(housing, cars, travel) will slow down due to uncertainty in the job market. Recent data of Car manufacturers shows that More care in Yard than showroom as of last month. One of the reasons for big boom in big ticket purchase was massive wage hikes in 2021-22. Similary, lilquidity is drying up and it will drag market more than expected. All the assets class have run up a lot in last few years and it definitely need a break and overhaulign of the system.

Valuations 1 year back were what they were at the top of 2018. So its only got more and more ridiculous as the market has gone up relentlessly and without any breaks. I've personally shifted from Mid and Small Cap to defensive funds a month back. My system says that profit which is not booked is not a profit. My Long Term targets of Indian market remains the same for 2030 and beyond but current level looks like a bubble where new clients want to onboard every now and then and bus seems to be over crowded.

Stay Safe, control on greed and take a pause to run farther in long run.

Regards,

GYC by Dinesh Aneja

Read More →

Category

Mutual Fund

Ever wondered how your daily choices shape India's economy? From the smartphone in your hand for groceries you buy, your decisions fuel a consumption revolution. Today I want to share why the Consumption Fund is a unique investment opportunity.

India is transforming rapidly, it's now the fifth largest consumption market in the world and with the country's per capita income crossing $2,000, we are witnessing a significant surge in consumption spending.

But what's fusing this transformation? Let's take a closer look. India's consumption story is booming. With rising incomes, more people are spending on a better lifestyle. As the largest young population in the world, with a median age of 28, India is driving a shift towards diverse product preferences.

By 2031, India will comprise 25% of the world's working population. This is leading to rapid urbanization as a large young workforce migrates to cities for better job opportunities and higher living standards. The burgeoning urban middle class is driving a consumption revolution, trading up to premium products and experiences.

E-commerce and digital payments are enabling this spending spree, catering to evolving preferences while easy access to credit is bolstering spending power. This consumption surge presents substantial investment opportunities. That's where the Consumption Fund comes in.

The fund's strategic investing sector poised to benefit the most from these trends, including autos, FMCG, healthcare, retail, power, and e-commerce. The fund focuses on quality companies with strong growth potential and actively manages a diversified portfolio to balance risks and results. The New Fund offers you a chance to be part of India's dynamic road story.

So, join us in harnessing the potential of one of the fastest growing economies and be a part of phenomenal Growtw by investing in the fund which can create wealth for you in long run.

Thanks

Read More →

Category

Personal Finance

**1. Goal is due / Target return is achieved** – There are investments which we make keeping a goal in mind (mostly in mutual fund or in bouquet of products). Such investments are ideally to be reviewed and monitored regularly and often get moved to less volatile products as the goal year is coming nearby. Then there are investments which are made keeping a target return in mind (mostly from investments in stocks). Exiting from all these planned investments should be a no-brainer provided you do not get greedy or fearful during such time.

**2. Non-performance / Change in strategy** – Such decisions often come out of a review meeting where your portfolio is analysed in detail. If certain investments in your portfolio have been consistently lagging in performance compared to peer group of products – then it could be the right time to exit and switch to some better alternatives. Or there may be a change in fund objective or strategy which is not fitting your requirements – then also exiting could be an option.

**3. Financial emergency** – Despite having a sizeable amount in emergency or contingency fund – there could be scenarios, where taking money out of the investments is the only option - we are left with. In such situations, though considering market level or outlook is secondary – but it is of primary importance to consider – which investment to part with. Consider the potential gain you are sacrificing, tax impact, exit load etc. before finalizing on which product to exit from.

Any time is good time to invest – this sentence has almost become a common parlance for all investors like us and largely for long-term investors – this is true also. But not many are talking about right time to take our money out of investments. Whether you consider redemption as a part of personal finance strategies or as a need – it makes lot of sense to know a thing or two about redemption.

Read More →

Category

Personal Finance

**Risk appetite** is how much risk an investor is ready / willing to take. On basis of his answer, we often mark him as an aggressive, moderate, or conservative investor. Based on only this criterion, if financial products are chosen – chances of going wrong is high. Why? Because such answers, given by investor, largely depends on – current market outlook, investor’s experience with some or other investment products, and finally, herd mentality that exists in that period. None of these are ideal or reliable ways to measure one’s risk profile. Even if we agree that investor is giving genuine, unbiased, and informed answers to risk profile questionnaire – still this may not lead to ideal and optimized investment decisions. What is the alternative then? The answer is – Risk Capacity.

**Risk capacity** of an investor is determined based on – individual financial net-worth, age, income level and above all the time horizon of the planned investment. Trusting risk capacity over risk appetite while finalizing on investment products – is often considered a better choice. Let us understand this with an example of cricket.

**Example 1:** Suppose, Team A, batting first, scored 199 runs in a 50 over match. Now, while Team B is coming to bat second – they can afford to not take any risk and keep a run rate of 4 per over should be sufficient. Here, even if Team B’s risk appetite is high, it makes sense to take a conservative or moderate approach to win the game (or achieve the goal).

**Example 2:** Suppose, Team A, batting first, scored 399 runs in a 50 over match. Now, while Team B is coming to bat second – they cannot afford to go slow as they must maintain a run rate of at least 8 per over. Here, even if Team B’s risk appetite is low, it makes sense to take an aggressive approach to win the game (or achieve the goal).

Relating this to personal finance, suppose a young investor of 30 years age (with not much of net-worth and surplus) is planning to achieve a long-term goal like retirement – choosing only low-yield fixed income assets for the same, will not be recommended – even if he is having a conservative risk appetite. Instead, he should take calculative exposure in well-managed equity assets as the goal is long-term and available surplus is not sufficient.

On the other hand, when the same young investor is planning to achieve a short-term goal like making a down-payment to purchase a house – choosing equity assets for the same will be a strict no-no. Instead, he should consider a non-volatile fixed-income instrument for the same.

The purpose of making investment may differ – going to an expensive vacation, foreclosing an outstanding loan, funding for children’s higher education or securing own retirement years etc. But while implementing any of these investment decisions – we must pick and choose some or other financial products. At this juncture knowing investor’s risk profile is said to be of paramount importance, which consists of his/her risk appetite and risk capacity. What is what? Let’s check. Read on.

Read More →

Category

Mutual Fund

**How IDCW (earlier known as mutual fund dividend) is different from stock dividend?**

When we receive a dividend from a stock we hold, it is sharing of profit earned by the respective company. When a company declares dividend on its stock, it does not bring down the stock price anyway. In layman’s term, we can refer receiving dividend from stocks as ‘extra income’ which is over and above the unrealized or realized gains we receive from holding that stock.

But in case of mutual fund, ‘dividend’ is compulsorily to be paid out from realized gains by the fund manager. So, paying out such ‘dividend’ of course results in a drop of its unit value or NAV as it is distributing income to certain unit holders (who opted for it) by withdrawing from its capital – thus the apt name for this activity is Income Distribution cum Capital Withdrawal.

**What is SWP (Systematic Withdrawal Plan) then?**

In case of SWP, fund manager has no role to play. Instead, you are at the driver’s seat. It is nothing but you are redeeming your units, irrespective of whether that means realizing gain or loss. In case of IDCW, it must come from realizing gains, no exception there. Also, declaring ‘dividend’ from a mutual fund scheme depends solely on the fund manager. It is up to him or her to decide, both the ‘dividend’ amount and frequency.

**How are SWWP and IDCW taxed?**

IDCW or ‘dividend’ income received from a mutual fund scheme adds to a unit holder’s income (under ‘income from other sources’) and therefore taxed accordingly. So, if you are in 30% tax bracket, you are then taxed accordingly. In case of SWP, it comes to you as ‘capital gain’ (short-term or long-term) and not as income for you. Now, we all know that short-term gain from equity mutual fund is taxed at 15% and long-term gain from equity mutual fund is taxed at 10% (beyond Rs. 1 lakh gain from equity holding in a financial year). So taxing of SWP income has nothing to do with what tax bracket you fall into.

**Conclusion**

If you want to receive regular income from your mutual fund holdings at your preferred terms – that is frequency and amount of income are decided by you – then go for SWP. The added benefit here is SWP’s tax efficiency over IDCW option.

Shakespeare said – What’s in a name? But in reality, naming a thing has lot to do with how we perceive a thing. Take, for example what we used to refer earlier (many of us still use that in casual terms) as ‘Dividend’ in a mutual fund. That time, it was often thought that dividend received from a mutual fund scheme is same as dividend received from a stock we hold, which it is not. To clear that confusion, SEBI rechristened it as IDCW (Income Distribution cum Capital Withdrawal). Did this rename help? Let’s see.

Read More →

Category

Personal Finance

First things first – gold itself should not be considered as an asset class, the right asset class in this regard could be ‘commodity’ as a whole. But the awareness and availability of other forms of commodity is still very rare and sparse. So, in that case if we consider gold itself as an asset class, then how it is placed against all other asset classes (e.g. equity, debt, real estate etc.)?

➜ Still in our country, gold is largely bought and kept in physical form and mostly in form of jewellery. It is somehow considered as holy, a part of social custom, an ideal gift on some occasions and above all – a status symbol. In all these cases, gold actually turns out to be a dead asset, as it is never sold neither it results in any sort of income stream. If you ignore the notional value of it and consider the cost of maintaining a locker to keep your physical gold safe, it even results in negative return.

➜ Off late, people started buying gold in digital form, where gold as a unit gets credited in your demat account like shares and bonds. Here, your holding reflects the gold price. So, when you decide to trade, equivalent amount of money gets credited in your bank account. With that money, you can then buy physical gold or spend in whatever way you want.

➜ Sovereign Gold Bond (SGB) tries to address this issue by giving you a regular income stream at the rate of 2.50% (taxable) p.a. payable half- yearly. If you hold the SGB till its maturity i.e. 8 years, then post maturity you need not pay any capital gain tax. After 5th year, you can sell it back to government on the date of interest payout. Anytime you sell it whether back to issuer or to a buyer (as it is tradable in exchange) after 3rd year and before maturity – you end up paying long term capital gain @ 20% with indexation (i.e. inflation factored in). Selling it before 3 years will attract short term capital gain tax as per your tax bracket.

Now the question is – should gold be part of your investment portfolio? The answer is – need not be in case of long-term goal-based investing. If your investment horizon is long term and you are overall bullish about India growth story and economy – you can very well keep predominantly equity and some percentages of debt asset.

If your investment horizon is medium term or short term and you are worried about economic downturn, rapid rise of inflation, Indian currency losing purchasing power – then you can very well consider gold as part of your investment portfolio.

But if your purpose is diversifying your portfolio to generate certain benchmark return, keeping 5 – 10% of gold asset in portfolio often proved out to be a good strategy. Of course, in such cases gold must be bought/kept in paper or digital form. Multi-Asset Allocation Mutual Fund schemes also offer a readymade solution in this regard and can be considered.

Should Gold be part of your investment portfolio? If yes, then how much? In that case, in what form should we buy gold – physical gold jewellery, bars, coin, Gold ETF or SGB (Sovereign Gold Bond)? Questions are many. As usual, in many other cases of personal finance, here also the answer is – “It depends”. But it depends on what and how much? Let’s discuss.

Read More →

Category

Personal Finance

**Deciding on Financial Roadmap** – This includes fixing a financial goal with definite time-period, target, and priority. This may sound simple but requires serious time and effort. Very few people do it with sincerity. This is either done in half-hearted casual manner or never done it at all. This exercise often gets postponed for ever. For example, finding out the current cost of education to plan for child’s higher education goal, is often not done properly. Even if the goals are fixed and planned, implementation of the same are often not done immediately or required investment amounts are compromised.

**Related Actions (e.g. review / documentation / technology)** – This is by far the most ignored area of managing personal finance by many. People rarely sit for a review session with their advisors in time. Also, the outcome of review is rarely followed by many. Still many investors do not include their family members in this journey. Documenting all investments and insurance in one place, is again an ignored area of action. Getting acquainted with latest technology, following its safety guidelines and best practices, are also overlooked unfortunately.

**Behavioural Finance** – In books or in insights shared by famous investors, it is frequently mentioned, that real wealth is created through long-term regular investing – but very few of us rarely practice this (unless we forget about an investment!). Though we are not supposed to compare the returns generated by our portfolio with others – still many of us do that and feel good or bad about this. Coming out of an investment is equally difficult for many of us – as either we feel greedy or egoistical about it.

The more seriously we follow the sermons of great investors – the better for us and our family. Let’s give it a try, once more. Never say never. All the best!

Like in every aspect of life, we behave quite differently in managing our finance than mentioned in books and in theories. Of course, those books are written for our benefits and those theories are formulated for our financial wellbeing, but still, most of us rarely could follow such guidelines ditto in our everyday life. How funny or contradictory it may sound, but it is the reality. Let’s discuss few such areas of personal finance where theories and practical implementations differ a lot. Again, such things cannot be said in general, as there are exceptions, but still such a discussion may hit us when we will tend to divert again, if ever, from the theory.

Read More →

Category

Taxation

**Tinkering with the horizon**

When an investment allows to claim deduction from your taxable income under some section, then it often comes with some lock-in period. In other words, you have to sacrifice liquidity for availing the tax benefits. This can be problematic. If you may need money in short-term, then locking-in majority of your investment will make you feel helpless and force you to take desperate measures. Or, if your financial goal may require money sooner or later than the pre-decided timeline – then you will be stuck with your locked-in investments.

**Ignoring Risk Profile**

If I say capital gains that you made from your equity investment is taxed much lesser or not even taxed at some situations compared to your investment in other asset classes (debt or commodity) – does that mean you ignore your risk profile, goal horizon and invest maximum in equity? You should not.

**Compromising Asset Allocation**

Investing separately in Gold Fund, International Equity Fund or Debt Fund is not that tax efficient. But that does not mean that you ignore your exposure in such funds and instead invest only in multi-asset allocation fund just because that is tax efficient (though that can be a topic on its own for some other day).

**What should be done?**

Give achieving your financial goal the topmost priority. Check your risk profile, consider your surplus, find out how much return you should earn – choose your asset class and investment product accordingly. If features of a tax saving product get perfectly aligned with your goal and risk-return profile – then of course go ahead and make that part of your portfolio. Otherwise not.

If your decision of making investment or choosing insurance policies has often been taken for the sole purpose of saving some tax – then you have reasons to worry. This tendency of jumping on the bandwagon i.e. saying ‘yes’ to a product just because it offers some tax saving can backfire or do harm to your overall portfolio of investments and insurance. Let us see, how.

Read More →

Category

Taxation

**SIP – Systematic Investment Plan**

It is a nice, convenient package solution for making repeated additional purchases in a mutual fund scheme. We need to choose a particular date of the month, how long we are going to invest and a fixed amount that should get debited from our bank account and get invested in the chosen scheme.

Through SIP investments, we purchase some units of the scheme in the current NAV i.e. price per unit. Now suppose, you are doing SIP in an ELSS (Equity Linked Saving Scheme). In that case, number of units that you buy in each SIP transaction, will remain locked for 3 years. So, if you do a 12 months’ SIP in an ELSS, you would be able to redeem all the purchased units only after the end of 4 years from the starting date of your SIP.

SIPs can be topped-up i.e. instalment amount can be increased after every 12 months. This is a very powerful and practical feature of SIP investment that not many investors exercise. This way a goal can be achieved with less strain on your pocket at start.

**SWP – Systematic Withdrawal Plan**

It is a nice, convenient **package solution for making repeated withdrawals** / redemption from a mutual fund scheme. We need to choose a particular date of the month, how long we are going to withdraw and a fixed amount that should get credited to our bank account and get redeemed from the chosen scheme. This will go on till the time your fund lasts or the mentioned fixed tenure – whichever is earlier.

Like step-up SIP, step-up or **inflation adjusted withdrawal** through SWP is not that straightforward, but still can be achieved with some minor adjustments and tweaking. But it makes perfect sense, that your withdrawal amount does not remain fixed, and you get to withdraw slightly larger amount after every 12 months to support the increased household and lifestyle expenses for instance.

Very few investors know / understand / realize that the entire withdrawal amount from SWP is not taxed but **only the resultant capital gain part**. Let me explain it. In every withdrawal, you redeem some number of units, say X. Now, these X number of units have some purchase NAV and as well as sale NAV. Your capital gain will thus be calculated as – Number of Units Redeemed * (Sale NAV – Purchase NAV).

**STP – Systematic Transfer Plan**