Recent Blog

Category

Behavioural Finance

Dear Investors,

I've been recieving lots of call now on Equity Market boom and how to increase my allocation in Equity as greed is at its peak. I share my perspectives on a topic, where investors will find useful. This time I delve into value and risk in investing during bull markets.

**A Stock Market Story**

Do you remember the atmosphere in the equity markets towards the end of 2007? The Sensex had been up about five times over the previous five years, and really, there was a madness in the air. There seemed to be no end to how high and how fast stocks could rise. We all remember how it ended, but that’s not my point today. My point is not what happened to the markets when they crashed but to individual companies when they recovered.

Whenever the markets rise like they did then, they eventually crash. It was inevitable then, and it’s inevitable now. There may be some doubt about when it will happen and by how much, but it will definitely happen. But correctly timing of such events is next to impossible. To a seasoned equity investor, this is nothing unexpected. Ups and downs are part of the game as I've seen 2 such major collapse in my life since I started my career in this industry in Jan 2004.

The part that few investors appreciate is that these are dangerous times. Over the next few years, when the dust settles in the next market cycle, you will find that these weren’t great times as far as buying stocks or Equity Mutual fund was concerned. You might think I’m saying this only because during bull runs, valuations are high, and stocks are expensive. You would be right, but that’s not the only reason and the biggest one. The biggest reason is psychological. When anything you buy makes money, the constant scepticism that investors need disappears from their brains.

This euphoria can lead to poor decision-making, where investors ignore fundamental analysis and chase momentum. They may overlook company financial or governance red flags, blinded by the allure of quick gains. Moreover, even mediocre companies can see their stock prices soar during these times, creating a false sense of security. It's crucial to remember that when the tide eventually turns, the quality of the underlying business will determine which stocks survive and thrive, not just market sentiment.

In fact, before the market peaks out, I read a newspaper column with this interesting story: One day, a man appeared in a village and offered to buy all the monkeys that the villagers could supply for Rs 1,000 each. The villagers caught all the monkeys around and sold them. Soon, another man appeared and offered Rs 2,000 for each monkey. However, there weren't any more monkeys around so that the villagers couldn't sell the man anything. However, they figured that, for some reason, the demand for monkeys was going up, so they looked for the first man and bought back all the monkeys for Rs 3,000 each (which was the least the man was willing to take). Unfortunately, this stratagem failed, and the buyer never reappeared, leaving the villagers stuck with the animals.

Nearby, there was another village where the same story was repeated, except it was about goats. The final buyer also never appeared, and the villagers were stuck with the goats. However, there was a big difference. The monkeys were a nuisance. They were noisy, troublesome, and dangerous, and they stole food all the time, so the villagers eventually abandoned them in the forest. The goats, however, were alright. They were easy to keep, grazed on grass and gave milk. When they grew older, the villagers slaughtered them for meat. All in all, buying goats was not the bad deal it looked like initially.

For investors in today’s raging bull market, the moral of the story should be obvious. In this heated market, take great care to differentiate between the 'monkeys' and the 'goats' in your portfolio. The 'monkeys' are the speculative stocks or mutual funds with very high return, hyped up by market sentiment but lacking fundamental value. When the market inevitably corrects, these stocks / funds may prove to be not just worthless but actively detrimental to your financial health. The 'goats', on the other hand, represent companies and mutual funds with with solid fundamentals, strong business models, and the ability to generate real value over time as they can contribute to India's growth story for many years from here on.

The goats are expensive, too, but at least they will deliver value even after buyers disappear. Start looking for goats and sell the monkeys for peace in life as you've already added many species in your Financial Jungle.

The story is sourced from [here](https://www.valueresearchonline.com/stories/10590/monkeys-goats-and-markets/)

Regards,

GYC by Dinesh Aneja

+91 8800 203200

Read More →

Category

Behavioural Finance

Greetings !!!

Have received many calls today post market fall. The fall was very much obvious and due basis the data in last few weeks. However, to answer all your questions, I've tried explaining on Exit Plan.

Any time is good time to invest – this sentence has almost become a common parlance for all investors like us and largely for long-term investors – this is true also. But not many are talking about right time to take our money out of investments. Whether you consider redemption as a part of personal finance strategies or as a need – it makes lot of sense to know a thing or two about redemption.

Following 4 things must be considered while making redemption from any investment:

1. Goal is due / Target return is achieved – There are investments which we make keeping a goal in mind (mostly in mutual fund or in bouquet of products). Such investments are ideally to be reviewed and monitored regularly and often get moved to less volatile products as the goal year is coming nearby. Then there are investments which are made keeping a target return in mind (mostly from investments in stocks). Exiting from all these planned investments should be a no-brainer provided you do not get greedy or fearful during such time.

2. Non-performance / Change in strategy – Such decisions often come out of a review meeting where your portfolio is analysed in detail. If certain investments in your portfolio have been consistently lagging in performance compared to peer group of products – then it could be the right time to exit and switch to some better alternatives. Or there may be a change in fund objective or strategy which is not fitting your requirements – then also exiting could be an option.

3. Financial emergency – Despite having a sizeable amount in emergency or contingency fund – there could be scenarios, where taking money out of the investments is the only option - we are left with. In such situations, though considering market level or outlook is secondary – but it is of primary importance to consider – which investment to part with. Consider the potential gain you are sacrificing, tax impact, exit load etc. before finalizing on which product to exit from.

4. Switch (Alternate Process): To make your portfolio more stable and protect the gains, it is advisable to rotate your holdings from Equity to Debt, Gold, International Market and other assest class. Retail investors usually enters in the last leg of rally and becomes long term investor. Idea should be to "Buy the Fear and Sell the Greed". If you follow above, you can become the next Warren Buffet of Investing community.

Feel free to connect regarding your portfolio discussion in coming days on +91 8800 203 200.

Jai Hind. Happy Investing !!!

Read More →

Category

Behavioural Finance

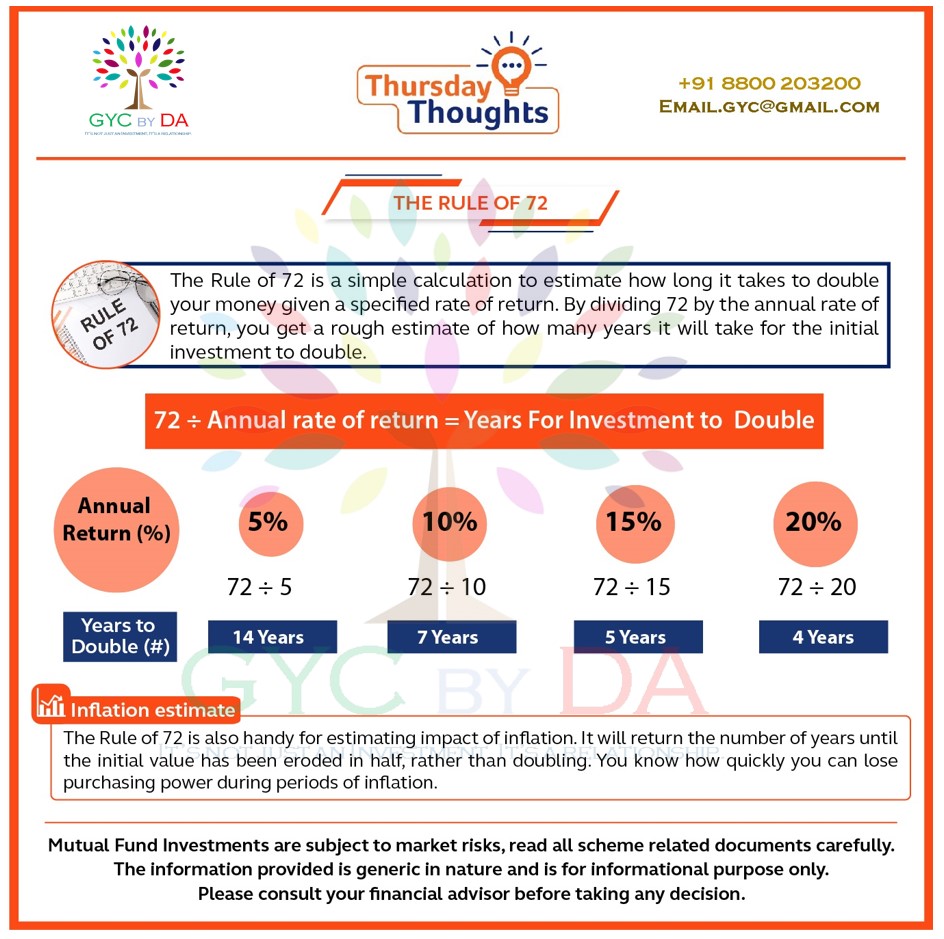

**In personal finance, many a times, we use certain quick and easy calculations to find out investment or insurance related insights. ‘Rule of 72’ is one such calculation method to find out how many years it would take to double our investment given a certain compounding rate of return. But how accurate is the result? Can you trust the result for critical high value calculation? Read on.**

Let’s start with an example of using Rule of 72. Say we are assuming that our investment will give a return of 9% p.a. Now if I invest Rs. 1 lakh in this product, by when my investment value would become Rs. 2 lakhs then? If we use Rule of 72, then we can find the answer the below way:

No. of years to double my investment = 72 / Given rate of return = 72 / 9 = 8 Years

So, after 8 years, my investment of Rs. 1 lakh will become Rs. 2 lakhs. Let’s verify this result with an Excel function viz. NPER:

=NPER(9%, , -100000, 200000,) = 8.0432 Years

The difference is of almost 15 days. Still the result is quite close compared to what we found using Rule of 72.

Now, let’s assume a higher rate of return e.g., 18% from my investment – rest everything remains the same. Number of years would take to double the money –

Using ‘Rule of 72’:

=72/18% = 4 Years

Using Excel NPER function:

=NPER(18%, , -100000, 200000,) = 4.1878 Years

The difference is now of almost 73 days. So, the accuracy of result is getting compromised here.

The conclusion is:

The ‘Rule of 72’ works well or serves the purpose in most cases. But if accuracy really matters for you, then you must remember that Rule of 72 works best or gives quite close to accurate result when the assumed rate of return is between 6% to 10%.

**Keep visiting us to know more such ideas!!!**

Read More →

Category

Behavioural Finance

“I am planning to go for a vacation every year with my family, starting from this year. Create a financial plan for that and let me know how much I should invest for the same?” – we often hear this from clients. Another similar request could be – “My daughter recently got admitted in this new International School. Expenses for the same would start from Rs. 1 lakh this year and so on for the coming years with inflation adjustments. Make sure that you include this in my financial plan.”

It really feels good when investors come forward and ask such questions or make such requests. This clearly implies that they are taking their personal finances seriously. But this begs another question – Can these be termed as financial goals? If a goal is to be achieved every year, including the current year or the next year – can that be planned then?

The answer is – NO. These are part of your cash-flow and budgeting. You must set aside an equivalent monthly amount from your regular income to meet such expenses. If that expense is not immediate, you can park that money in some liquid and safe investment for the next few months – that’s it. So, such cash outgo is part of your recurring expenses and cannot be or should not be termed as financial goals. These recurring expenses need not to remain constant over the years and may rise – so is your income. Remember, almost all recurring expenses are subject to inflation except a few like life insurance premium payments etc.

Is not retirement goal similar? There, we are also supposed to spend a certain amount every year – inflation adjusted. But retirement expenses are different from annual vacations or school expenses for two reasons – first, because retirement expenses are not getting started immediately and second, there will be no regular income coming then. That requires some serious planning, no doubt. But if you are planning a Europe tour or world tour after few years, then that is surely a financial goal to be planned.

Read More →

Category

Behavioural Finance

Check below 10 statements. If any one of these or more sounding familiar to you, then you have reason to worry.

1.Someday, I will tell my spouse / family members about all my investments and insurance. But not today.

2.Someday, I will find some time to store all my online credentials (e.g., passwords, PINs) in a better and safer way for my digital wellbeing. But not today.

3.Someday, I will make sure that all my data (be it in laptop or phone) is properly backed-up and synced through some cloud service. But not today.

4.Someday, I will gather all necessary information about my investment / insurance and put it in one place. But not today.

5.Someday, I will take some time out to meet my financial advisor to discuss / implement necessary steps for my financial wellbeing. But not today.

6.Someday, I will top-up my health insurance cover, as there are changes in my lifestyle and health status. But not today.

7.Someday, I will start / increase my SIP investment to achieve some of my financial goals. But not today.

8.Someday, I will start working on some better diet plan or some daily physical exercise. But not today.

9.Someday, I will make some investment in myself - maybe for my career growth or for nurturing a hobby / passion. But not today.

10.Someday, I will find a way to spend more time with my family. But not today.

Read More →

Category

Behavioural Finance

We all know and agree that to create wealth, we need a sane and logical mind above everything else. If we let our prejudice and emotions take over our rationality – that will most probably not turn out well for our wealth journey. Still, we see such mistakes happening in and around us. This may have something to do with our financial background, upbringing, tradition and peer pressure.

**Buying property as an investment**

This excludes buying the first property or the primary property to reside, though it can be proved, that most of the time, taking a property on rent near to your work location makes more financial sense than buying a property far away. This is even more true for those who already reside in their ancestral home there or for those who have come to a different city for work and not going to stay there forever. Still, even such people, on drop of a hat, go for buying a property right out as their first big investment(?).

Then there are those who buy second or third property for investment purpose. Such properties are also often bought on loan. Paying interest often outweigh the tax benefit that they enjoy. Also, for making any investment decisions – we must first consider 3 topmost priorities – return expected, liquidity and convenience (or maintenance). How property as an investment, scores in these 3 metrics?

**Return expected** – Barring few exceptions, average return from property investment ranges between 8 – 10%. Holding period varies a lot, but mostly not less than 5 years. Thus, this question arises in logical mind – don’t we have investment product which gives similar return in the same period with much better regulation, choices, transparency and liquidity? Net return from property also must consider interest payment, maintenance cost, brokerage cost, capital gain tax and so on.

**Liquidity** – This is almost a no brainer to categorize property as a highly illiquid product. Selling a property can never be planned on exact terms. There are so many moving parts. The process of finding a buyer, the legal works involved, the terms and delivery of payment – all these take their sweet time to complete. Also, you cannot part-sell a property, right?

**Convenience** – First limitation comes here from geographical boundaries. May be in some corner of the country, property prices are set to rise in big terms. But can we buy and maintain such property there sitting at the convenience of our home? No. How many of us ever bother to find the right price or intrinsic value of a property based on different parameters? Almost none of us. Can we find such analysis done by some experts for the selected property? Again, the answer is no. Can we buy / sell property completely online? Of course not. Can we be completely sure of all paperwork and legal formalities done as required by the builder / developer? We all know the answer.

So, on the above 3 metrics, property as an investment does not score well. This is by no means saying that property as an asset class is not good to invest. If you are a seasoned property investor, this may be the right choice for you. But is this the right choice for long-term investment for all of us? Is it worth taking the plunge? Do we have better options out there? How about giving that a rational thought – keeping emotion and peer pressure out of the way?

To be continued…

Read More →